Key takeaways

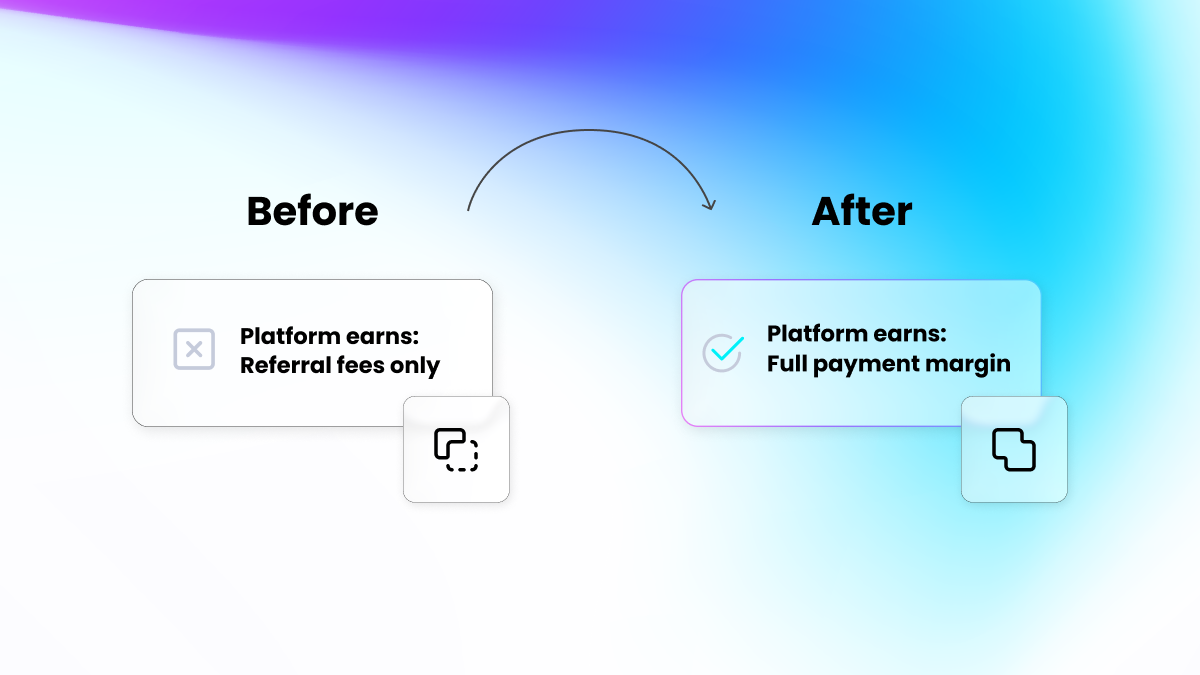

- Embedded payables let vertical SaaS platforms run automated vendor payouts inside their product, turning every outbound payment into a revenue stream for the platform and a faster, fully branded payout for the software customer.

- B2B ACH (electronic bank-to-bank payments) volume grew nearly 10% in 2025, with close to 8.1 billion B2B payments as businesses continue moving away from paper checks. That volume is the wave that embedded payables ride.

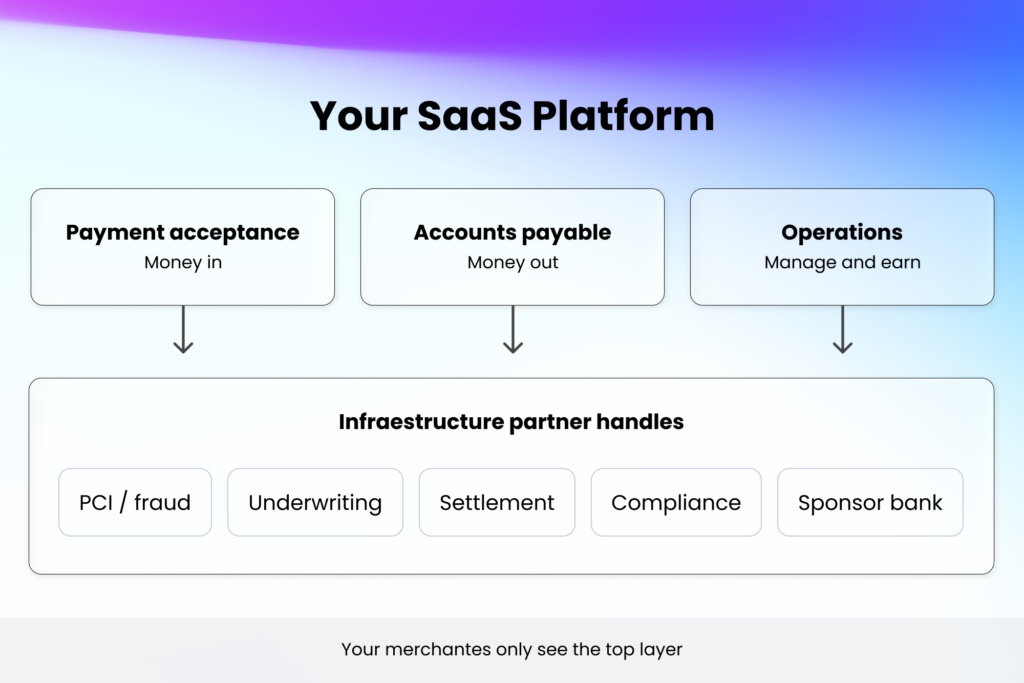

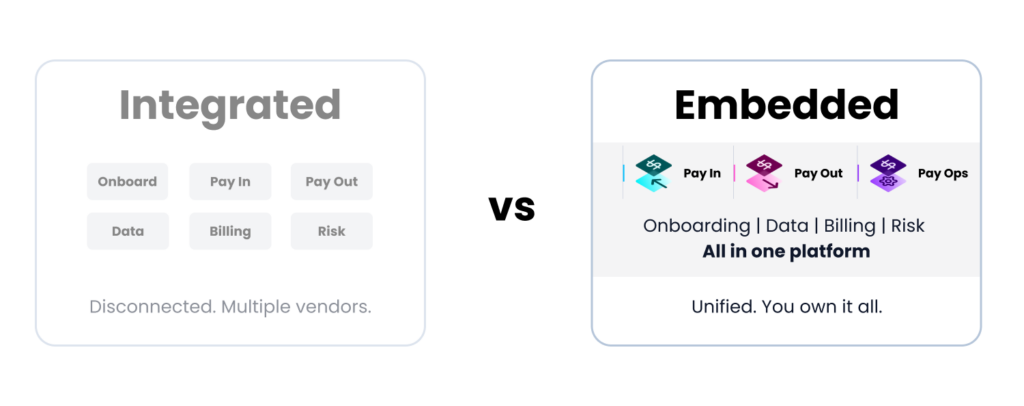

- A single API that covers payment acceptance, accounts payable, and payment operations keeps margin, data, and reconciliation under one roof, so adding accounts payable later does not mean onboarding a second vendor or rebuilding your reporting layer.

- Owning the outbound side gives the platform a complete view of money flowing through the software customer’s business — in and out — in one place.

Embedded payables let vertical SaaS platforms earn on the money their software customers send out, not just the money they collect. Vendor and subcontractor payouts still run through bank portals, AP tools, and paper checks that the platform never sees. This guide covers how the model works, what platforms earn on each rail, and what to evaluate in a partner.

What are embedded payables for a SaaS platform?

Embedded payables are vendor disbursements that run inside your SaaS product instead of outside it. The software customer approves a bill, the system pays the vendor through the rail the vendor prefers, and the platform earns on the transaction. The per-transaction margin, the vendor data, and the workflow all stay with the platform instead of routing to a third-party tool.

This is the half of embedded B2B payments that most vertical SaaS platforms have not yet captured. Acceptance (Pay In) was the obvious first move because software customers were already collecting money. Payouts are where the software customer’s weekly workflow actually lives, which is exactly why owning them changes the platform’s relationship with its customer.

Where embedded payables show up in a vertical SaaS workflow

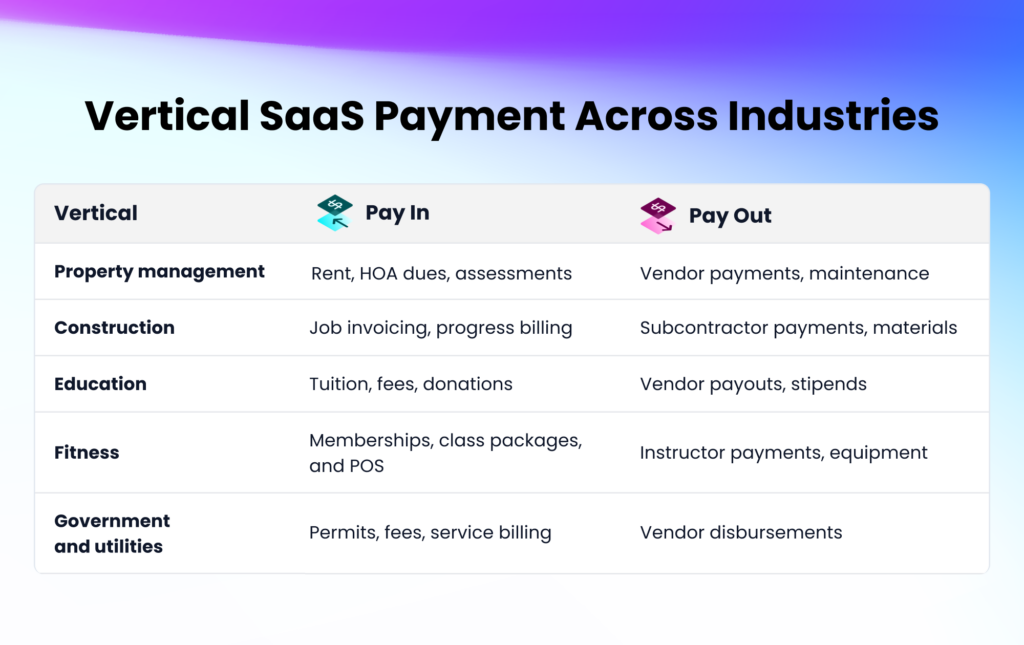

The pattern is the same across need-to-pay verticals, just with different vendors at the end of the line. A property management platform pays HOA service vendors and association contractors. A construction platform pays subcontractors and material suppliers on weekly draw schedules. A utility billing or field service platform pays the technicians and crews completing the work order. In every case, the payout sits one click away from the workflow the software customer is already using, and the mechanics behind that one click are what turn it into platform revenue.

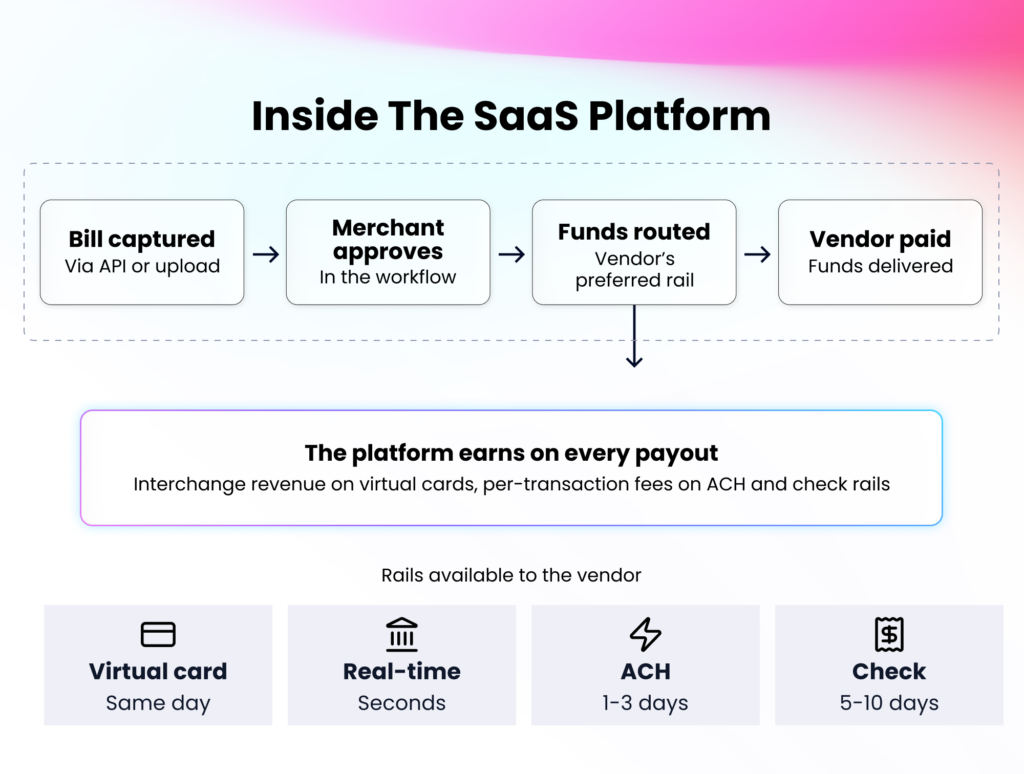

How do automated vendor payouts work for SaaS?

A bill enters the system, the software customer approves it, the payment routes through the vendor’s preferred method, and the data posts back to your platform with full remittance details. One API handles the money movement, webhooks fire at each status change, and the activity flows into the same reporting as your acceptance side.

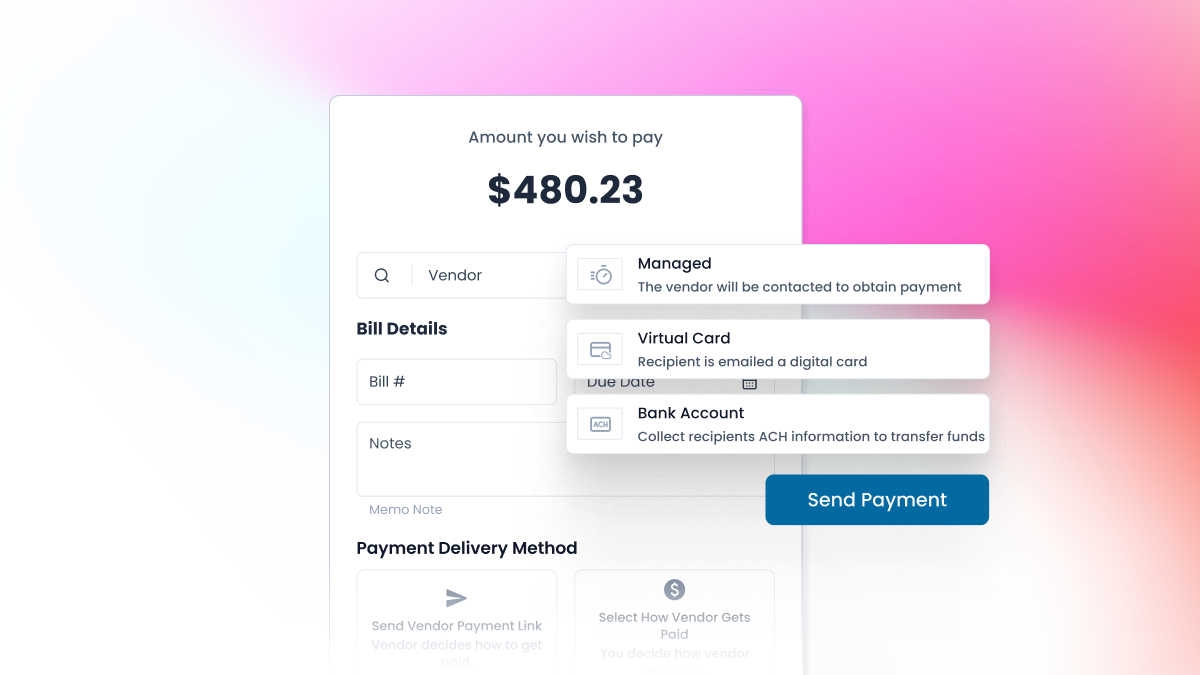

How does money move from your platform to a vendor or subcontractor?

Funds debited from the software customer’s bank account move through whichever rail the vendor accepts (virtual card, ACH, check, RTP, and wire transfers), and settle to the vendor through the partner’s custodial account. ACH (Automated Clearing House) is the bank-to-bank network most vendor payments still ride on. The software customer sees the same status the platform sees, in near real time, without leaving your product.

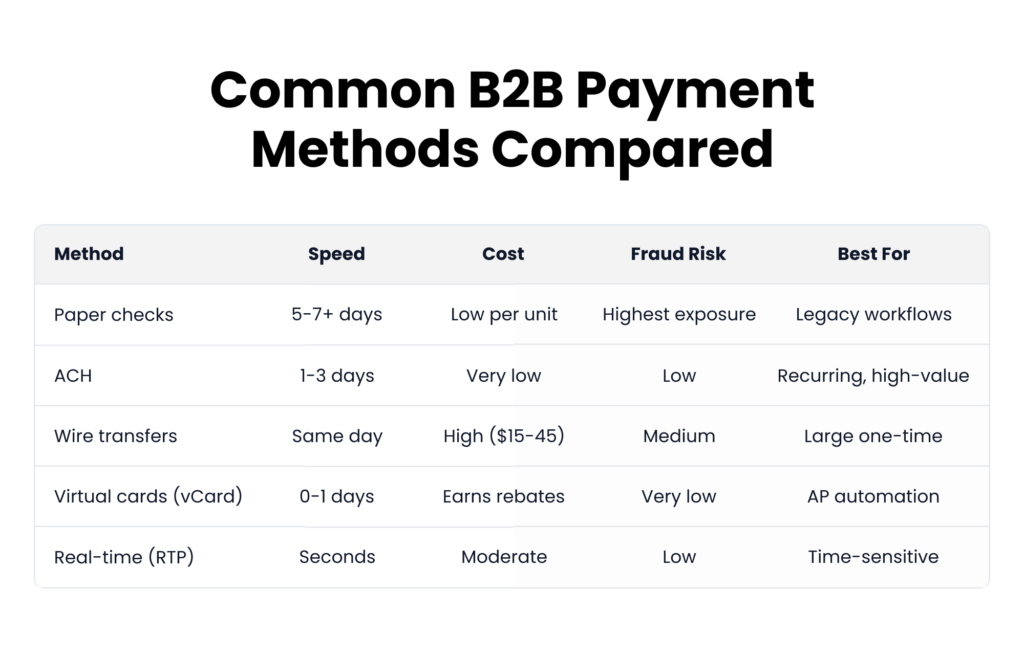

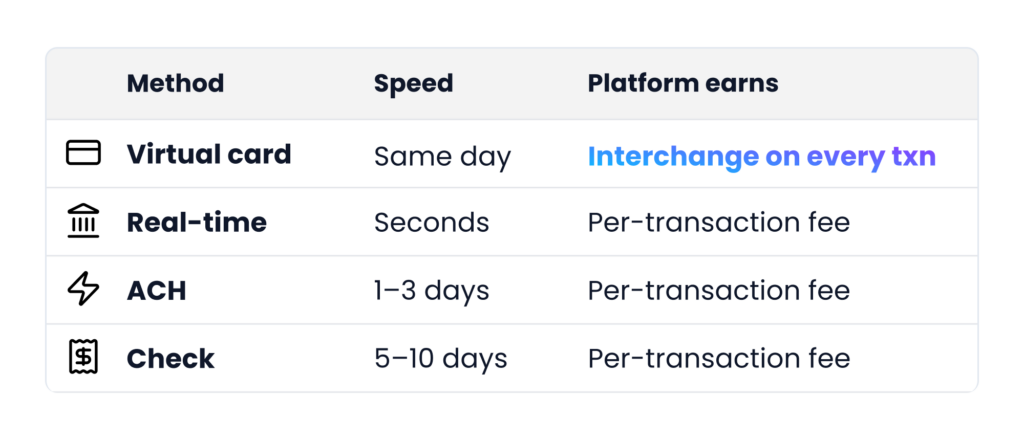

What payment methods can vendors actually receive?

Vendors can be paid through five rails, each with a different speed and platform revenue:

The shift toward digital rails is well underway. According to Nacha, B2B check usage fell from 81% in 2004 to 26% in 2024.

Virtual cards are digital card numbers issued for a single payment or vendor, and every transaction earns the platform interchange, a small percentage of the payment amount. For recurring vendors, Ghost Cards extend that earning model across the full year.

Who handles vendor enrollment and onboarding?

The embedded payments infrastructure partner runs vendor enablement through the product. Onboarding new payees is a configured workflow inside your software, not a manual process for your software customers or a support ticket for your team. Software customers focus on approving payments, not chasing banking details.

For situations where self-service makes more sense, Vendor Payment Links remove the enrollment step entirely. Your software customers send a secure link, the vendor enters their payment details, and funds are disbursed automatically. Collection and disbursement happen in one flow, with no portal to maintain and no enrollment to chase.

What are the benefits of embedded payables for SaaS platforms?

Four benefits drive the case for embedded payables: outbound revenue, stronger software customer retention, transaction data the platform owns, and a vendor experience under your brand.

1. Direct revenue on outbound volume

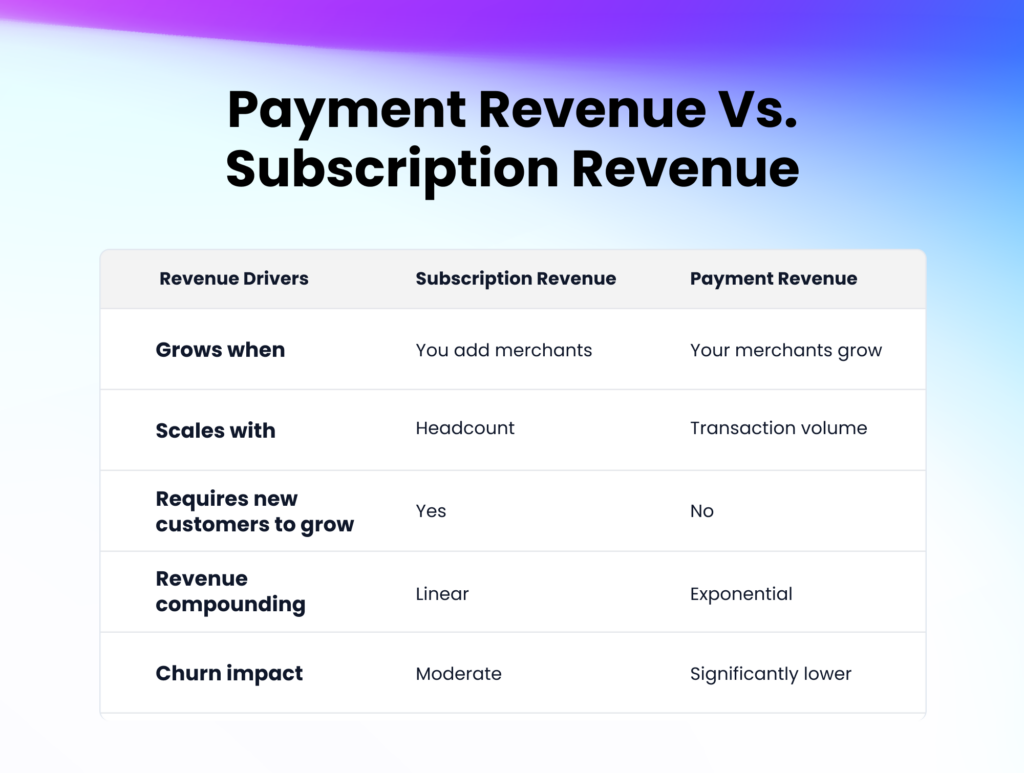

Every vendor payment earns the platform something. Virtual cards return interchange. ACH, checks, and instant payments return per-transaction fees. For most B2B software customers, outbound volume rivals inbound, which doubles the addressable revenue per customer.

2. Higher net revenue retention (NRR)

Approving bills, managing vendors, and reconciling payments are weekly tasks. When they run inside the software, the platform stops being a tool and becomes a workflow, which is what protects NRR.

3. Transaction data the platform owns

Every payout records which vendor was paid, when, on what terms, and through which rail. That dataset is what unlocks future products like cash flow forecasting, vendor scoring, and working capital.

4. A branded vendor touchpoint

Vendors get paid through the rail they prefer and see the platform’s brand on the remittance. The software customer looks more professional to their own vendors, and the platform’s brand reaches beyond its direct customer base.

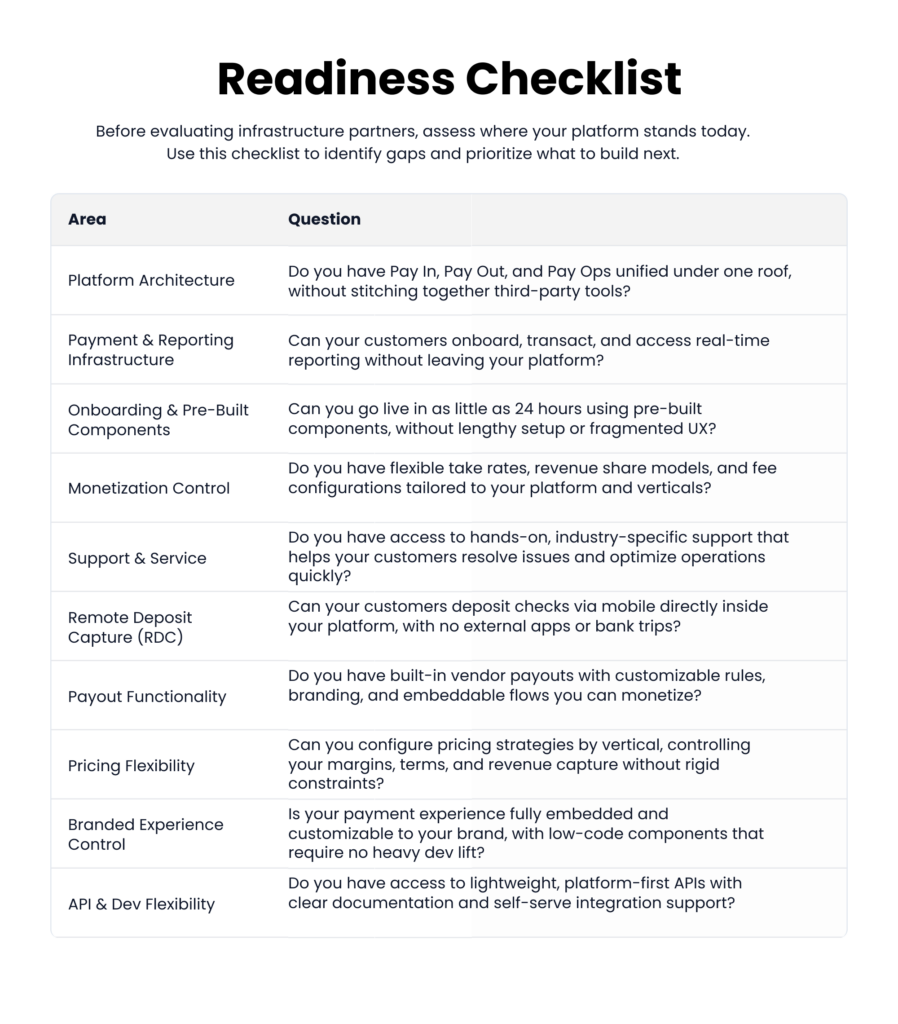

What should you look for in an embedded payables solution?

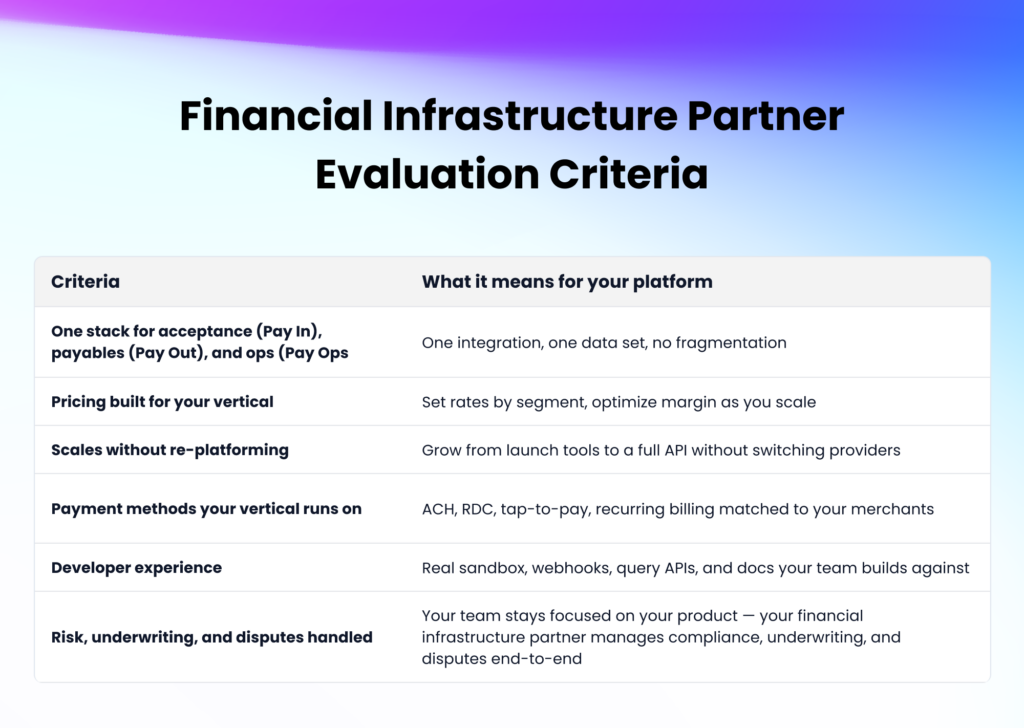

The right embedded payables partner protects your margin, your brand, and your software customer relationship. Three questions cut to whether one fits.

Does it handle vendor enrollment without adding work to your team?

A strong partner runs vendor enablement inside the product, so onboarding new payees is a configured workflow rather than a manual lift for your software customers or a ticket queue for your support team. Enrollment is also where virtual card adoption is won or lost, because every vendor who never gets enrolled is a vendor who keeps getting paid by check, which is the lowest-margin rail on the stack.

Does it support the rails your vendors actually want?

Virtual cards earn the most, but vendors will still ask for ACH and checks. A solution that supports all three lets your platform earn across the full rail mix instead of forcing every vendor onto one method. Real-time payments and wire transfers are the next rail to evaluate, because instant settlement is becoming table stakes in verticals like construction and field service, and the platforms that support it earn on a transaction tier their competitors cannot match.

Does it cover payment acceptance and accounts payable on one stack?

If acceptance is already live, the accounts payable layer should plug into the same API, the same reporting, and the same reconciliation. Splitting them across two vendors fragments software customer pricing, doubles the engineering surface your team has to maintain, and leaves no single partner accountable when margin or reconciliation issues come up. The unified stack is also what makes future products like cash flow forecasting and working capital monetization possible, because both sides of the software customer’s money flow are sitting in one dataset under your control.

How to add embedded payables to your SaaS platform

The integration choice shapes how fast you ship and how much engineering you spend doing it. The right path depends on engineering bandwidth, brand control needs, and how fast you want to start earning on outbound volume.

What integration options can you choose from?

Embedded payables ship through multiple integration paths, ranging from fully custom API builds to prebuilt, ready-to-launch options. Each varies in time to launch, level of UX control, and the engineering investment required. Your provider can walk you through the options that fit your team’s capacity and timeline.

Sunbound launched embedded payments with a single developer and one project manager in under two months and now processes over $1 billion in annual payment volume. For a deeper look at how to sequence the integration, see embedded payments best practices.

How do you pick the right path?

The answer is to pick the path that gets you to live software customers fastest, then upgrade later. Revenue on outbound volume only starts compounding once real payments are flowing, and waiting for a more complex build means months of forgone interchange. Most platforms that start lean ship significantly faster than the ones that try to build everything upfront.

What does your team focus on during rollout?

The provider handles compliance, sponsor banking, and risk monitoring. Your team focuses on the product decisions: who can approve payments, how funds are sourced, what the vendor experience should look like, and how reporting surfaces inside your existing dashboards. Most rollouts run on a weekly cadence with the partner during the build phase, then taper to monthly check-ins once the integration is live and software customers are flowing through.

How Payabli turns vendor payouts into a revenue stream for SaaS

Payabli offers payment infrastructure and monetization for vertical SaaS platforms. Our Pay In / Pay Out / Pay Ops framework unifies payment acceptance, accounts payable, and payment operations under a single API, so platforms capture both sides of their software customers’ money flow without managing multiple vendors or rebuilding their reporting layer.

Virtual cards, ACH, checks, real-time payments, and wire transfers are embedded alongside acceptance flows on the same integration. Vendor enablement, invoice intake, and configurable approval workflows are built in, so software customers see a polished, fully branded product from day one.

Vertical SaaS platforms in property management, construction, utilities, education, and government use Payabli to turn vendor payouts into platform revenue.

If you are mapping where embedded payables fit on your roadmap, book a demo to see what your platform’s payout volume could earn.