Key takeaways:

- SaaS platforms monetize payments by owning the infrastructure that their merchants already use to collect and send money. Every transaction becomes a revenue event instead of a cost.

- Adding payments to your platform can increase revenue per user by 2 to 5 times without adding a single new customer.

- The full revenue opportunity sits across three layers: payment acceptance (Pay In), accounts payable disbursements (Pay Out), and pricing tools (Pay Ops).

- The most common monetization failures: too many vendors splitting your margin, a lack of outbound payment strategy, and infrastructure not built for your specific vertical.

Your platform already has transaction volume running through it. Every invoice your merchants send, every transaction they collect, and every vendor payment they make is value your platform unlocks but does not capture. The margin on those transactions exists whether you capture it or not. Right now, a payment processor is keeping it.

This guide shows you where that revenue sits, what it takes to own it, and how to implement it without a multi-year engineering project.

What does it mean to monetize payments for a SaaS platform?

Most SaaS platforms already process payments. Most leave the revenue from them on the table. The difference is not technical, but it is who owns the margin. When a third-party processor handles your transactions, they keep the spread, the data, and the merchant relationship. When you own the infrastructure, you keep all three. The right time to make that shift is before your transaction volume becomes someone else’s moat.

How do payments become a revenue stream?

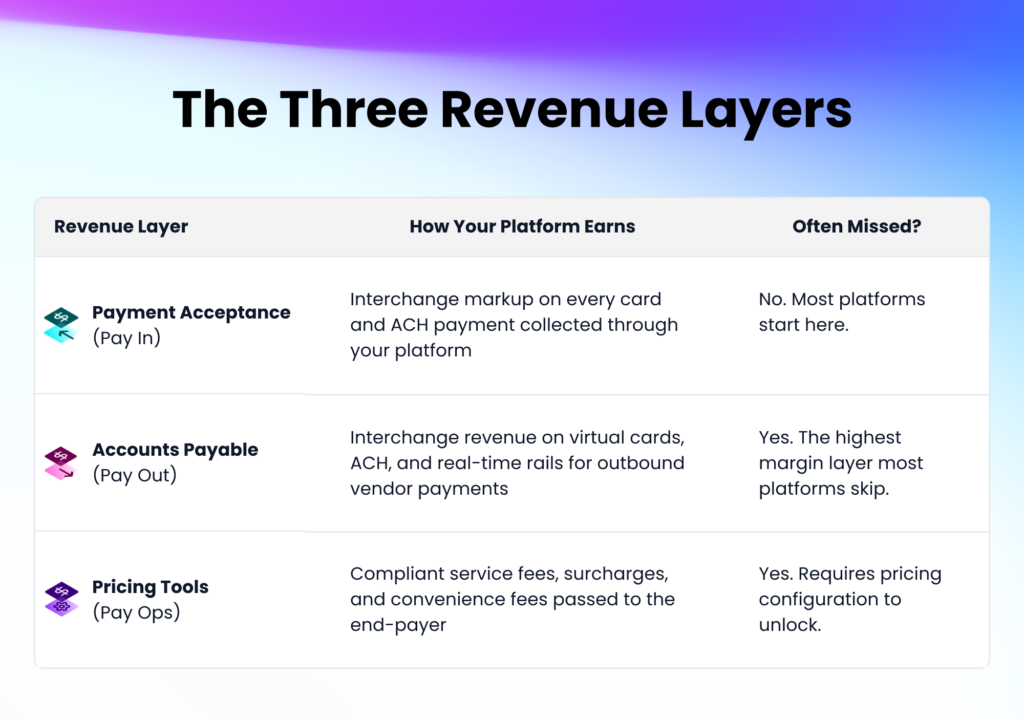

Your platform earns across three layers once you own the infrastructure.

The first is the transaction spread on payment acceptance. Every time a merchant collects a payment, there is a difference between the card network cost at the floor and what the merchant pays to accept it. Your platform retains the margin per transaction through interchange-plus pricing, and passing Level II and Level III data on B2B transactions qualifies those payments for lower interchange categories, widening your margin further.

The second is accounts payable disbursements. When your merchants pay vendors or subcontractors through your platform via virtual cards, real-time rails, or ACH, your platform generates interchange revenue on each outbound payment. This is often the most profitable layer and the one that most SaaS platforms overlook. It also opens the door to a broader embedded fintech stack.The third is the payment experience itself. Merchants pay for capabilities that remove friction in their operations: faster invoice collection, auto-reconciliation, and customer payment portals that cut support overhead.

Here is what the three earning layers look like in practice:

How can SaaS platforms benefit from payment monetization?

When you own payments, three things change in your business at once: how fast revenue grows, how hard you are to replace, and how you compare to platforms that have not made this move yet.

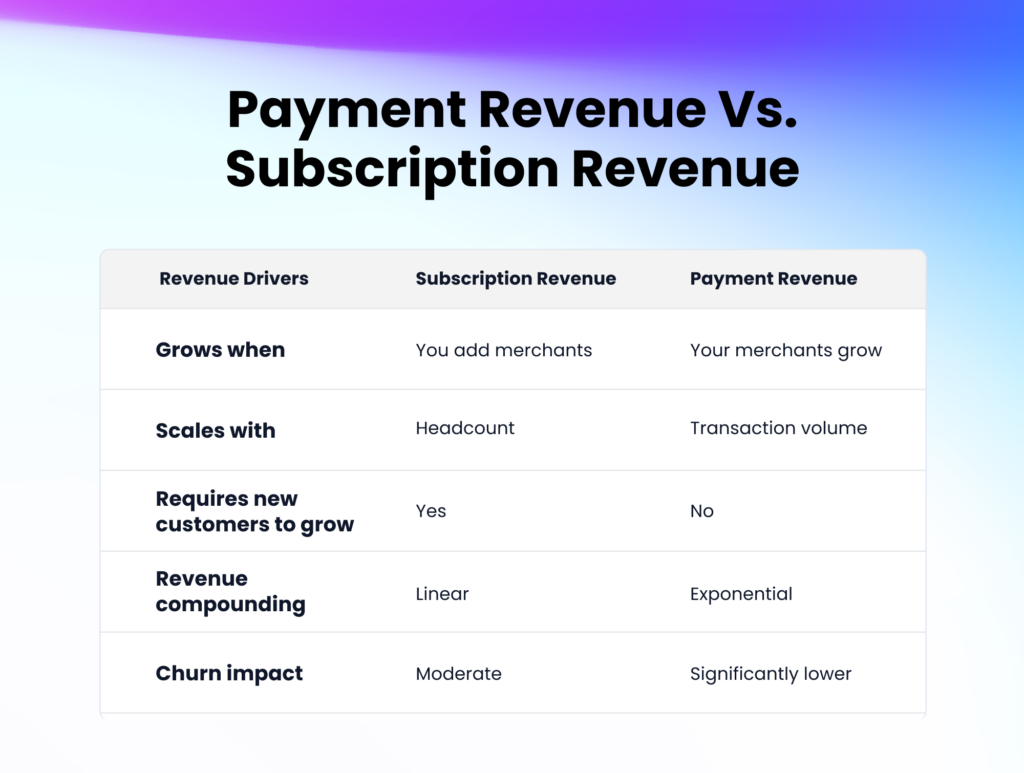

- Revenue that scales with your merchants. Your subscription revenue grows when you add merchants, whereas your payment revenue grows when your merchants grow. A merchant processing more volume generates more revenue for you automatically, with no upsell and no new contract required.

- Lower churn, higher retention. Payments embedded in a merchant’s workflow become essential to how they operate. The more transactions they run through your platform, the harder it is to replace you with anything else.

- A competitive position that is harder to replicate. Shopify’s 2024 annual filing shows its Merchant Solutions segment, which includes payments, shipping, and capital products now accounts for 73% of total revenue.

- Toast ended 2024 with $4.1 billion in payments and fintech revenue versus $706 million in subscriptions. For both, payments eventually became the business. Subscriptions became the acquisition channel.

The market is moving toward you. The payment volume is already shifting toward software platforms that sit inside merchant workflows. Juniper Research predicts embedded payment transaction volume will hit $2.5 trillion by 2028, a 134% increase from 2024. The platforms moving now are capturing volume that will be structurally difficult to take back later. Waiting is not a neutral decision.

How does payment revenue compare to subscription revenue?

The difference is not just in the margin. Subscription revenue is linear by design, it grows when you add merchants. Payment revenue compounds automatically because it grows when your existing merchants grow. Here is what it looks like side by side.

How can a SaaS platform effectively monetize payments?

Most platforms pick a vendor before they know what they are actually monetizing. That is where things go wrong. Start here instead.

Step 1: Map your payment flows

Start with scope, not technology. Where does money enter your platform, and where does it leave? Which flows are already happening outside your product that merchants would prefer inside it? This tells you how large the opportunity is. If you find more than two payment flows happening outside your product, you have enough volume to start monetizing now.

Step 2: Choose a suitable integration path

Once the scope is clear, the integration choice is straightforward. Full API for teams that want complete control. White-label portal and no-code components for platforms that want to go live with minimal engineering lift. Pick based on your team’s capacity. If you are weighing full PayFac registration against PayFac-as-a-Service, these common myths are worth reading.

Step 3: Build a merchant-oriented pricing model

This is where most of the revenue is won or lost. A blended flat rate is simple but leaves margin behind. Interchange-plus is more transparent and competitive at scale. The right model depends on your vertical and how price-sensitive your merchant base is, and getting it right is easier when your payments infrastructure provider understands the nuances of your industry and can help you price to maximize both adoption and margin

Step 4: Prioritize adoption from day one

Most platforms launch payments and wait for merchants to find them. That is the wrong sequence. Adoption has to be the default, not an option. That means payments surfacing inside the workflow at the moment a merchant creates an invoice or pays a vendor, not buried in a settings tab. Concretely: set your payment flow as the default on merchant onboarding, trigger in-product nudges when a merchant completes a transaction outside your platform, and track activation as a product metric from day one. The right payments infrastructure partner will also come with a point of view on all of this, from the adoption benchmarks that matter in your vertical to the KPIs worth tracking as you scale.

What should you watch out for when monetizing payments for SaaS

Technology is rarely the problem. Most platforms that underperform here make the same three mistakes. All three are avoidable if you know what to look for.

Are there too many vendors or margin leakage?

Every vendor in your payment stack takes a cut. Separate tools for onboarding, acceptance, disbursements, and reporting mean fragmented margin, integration debt, and data you cannot act on. A single API covering payment acceptance, accounts payable, and payment operations keeps those economics where they belong, with your platform.

What’s happening on the outbound side?

If your merchants are paying vendors through external tools, you are leaving revenue on the table and handing retention to another platform. The outbound side is where the next layer of margin lives and where most SaaS platforms have not looked yet.

Does my infrastructure work for my vertical?

Generic payment infrastructure is built for horizontal platforms or use cases, not your merchants’ actual workflows. Property management software needs lockbox collections, field services needs remote deposit capture (RDC) and utilities need ACH billing. The right infrastructure for a vertical SaaS platform is purpose-built for these need-to-pay workflows.

How can Payabli help SaaS platforms monetize payments?

Payabli gives vertical SaaS platforms a single API that unifies payment acceptance (Pay In), accounts payable (Pay Out), and payment operations (Pay Ops), so your platform earns on both sides of money movement without the compliance burden or capital requirements of full PayFac registration.

Platforms that have made this move see it in the numbers. Builder Prime reported a 1,000% increase in payment volume after embedding payments, with payments becoming a core retention driver. Sunbound went from 50% to 90% payor adoption in under a month after moving payments inside the product.

Book a demo to see what the economics look like for your vertical.