Key takeaways

- PayFac-as-a-Service offers vertical SaaS platforms PayFac-level merchant ownership, pricing control, and white-labeled branding without the 12 to 18-month registration period or full compliance obligation.

- Payment processing revenue through software vendors in the U.S. has grown at 20% annually, reaching an estimated $16 billion in 2025 (McKinsey).

- With PayFac-as-a-Service, the platform controls merchant pricing, onboarding, and the merchant relationship while the infrastructure partner manages sponsor bank relationships, regulatory compliance, and underwriting.

- The right PayFac-as-a-Service models unify payment acceptance (Pay In), accounts payable (Pay Out), and payment operations (Pay Ops) through a single API, giving platforms a complete payments business.

Every vertical SaaS platform eventually reaches a turning point where subscription revenue no longer suffices to fund the next stage of growth, while the payment volume flowing through the platform emerges as a revenue opportunity greater than the software itself. The next move is to become a payment facilitator, the entity that onboards sub-merchants, earns a margin on every transaction, and controls pricing. Full PayFac registration is the more resource-intensive route, requiring significant time, infrastructure, and compliance overhead. PayFac-as-a-Service is a faster path to the same revenue opportunity, without the organizational lift of becoming a registered PayFac.

In this blog, we will walk you through everything you need to know about PayFac-as-a-Service and how vertical SaaS platforms can embed payments, capture transaction revenue, and go live – while preserving the option to graduate to a registered PayFac when the time is right.

How do PayFac-as-a-Service and SaaS platforms work together?

For SaaS platforms, PayFac-as-a-Service is the unlock: embed payments into the product, own the sub-merchant relationship, and earn revenue on every transaction customers process without building the underlying infrastructure. Payment processing revenue through U.S. software vendors is projected to reach $16 billion in 2025, growing at 20% annually (McKinsey). Most of that margin is not going to the platforms generating value.

A Payment Facilitator (PayFac) holds a master merchant account with an acquiring bank, onboarding sub-merchants under it, and earning a margin on every transaction. Full registration delivers that control but takes 12 to 18 months and significant capital to get there.

PayFac-as-a-Service splits the model between two parties. The provider manages the sponsor bank relationship, compliance, regulatory reporting, and processing infrastructure. For a SaaS platform, this means payments live inside the product: the platform configures sub-merchant onboarding, sets pricing, controls the payment experience, and earns on every transaction processed, without building or maintaining the infrastructure behind it.

PayFac-as-a-Service vs. Registered PayFac for SaaS providers

Full registration and PayFac-as-a-Service deliver the same sub-merchant economics. What separates them is time, capital, and compliance overhead.

PayFac-as-a-Service vs. Full PayFac: Which suits your SaaS platform?

Full registration is typically suited for platform processing at scale, with the internal resources to manage ongoing compliance requirements. For vertical SaaS companies in property management, field services, education, utilities, and government, PayFac-as-a-Service delivers the same economics without pulling engineering resources away from the core product, while preserving the option to graduate to a registered PayFac when the time is right.

Why are SaaS platforms adopting PayFac-as-a-Service?

PayFac-as-a-Service adoption among vertical SaaS platforms has accelerated sharply, fueled by two driving factors: the revenue opportunity is too large to leave on the table, and the sub-merchant experience gap is becoming a retention problem.

Payments revenue without the compliance burden

Over 90% of U.S. sub-merchants now use an ISV solution for payments or business management, per McKinsey’s 2025 ISV maturity analysis. Platforms on a referral model earn a small fee for directing sub-merchants to a third-party processor. Platforms on PayFac-as-a-Service capture the margin between wholesale and sub-merchant rates on every transaction. A platform processing $100 million annually at 100 basis points generates $1 million in transaction revenue without adding a single customer.

The compliance argument is equally clear. Full registration requires a Qualified Security Assessor (QSA) audit for PCI Level 1, NACHA compliance, sponsor bank approval, KYC/KYB on every sub-merchant, and ongoing chargeback management. Platforms that stay on referral models also lose access to Level II and Level III interchange optimization, meaning they pay more per transaction than they need to while earning nothing on the volume. PayFac-as-a-Service removes the compliance burden and unlocks the margin optimization that referral models never could.

A branded sub-merchant experience you control

When a third party handles payments, sub-merchants onboard outside the platform, see a different brand at checkout, and contact a different support team for issues. The platform loses visibility into the payment lifecycle, and there is no way to fix the experience gap that the sub-merchant notices. With PayFac-as-a-Service, payments are white-labeled inside the platform. The experience is smooth, the relationship stays with the platform, and sub-merchants processing payments inside the software are significantly harder to churn. That retention shows up directly in net revenue retention numbers and valuation multiples.

The data cost is just as high. Without embedded payments, reconciliation stays manual, reporting lives outside the platform, and sub-merchants never get the payment visibility they expect from software they rely on daily.

What do I look for in a PayFac platform as a SaaS provider?

Not every PayFac-as-a-Service provider is built for vertical SaaS. Some are horizontal processors that have retrofitted embedded payments as an add-on. Here are the factors that separate a purpose-built infrastructure partner from a generic one:

Pay In, Pay Out, and Pay Ops under one roof

Practically, a complete PayFac-as-a-Service solution covers three areas: payment acceptance (Pay In), accounts payable (Pay Out), and payment operations (Pay Ops). The platform gets revenue from both the inbound and outbound payment flow, while the provider handles onboarding, risk, billing, compliance, underwriting, and reporting behind the scenes.

APIs and no-code options for faster integration

The strongest models offer a full API for maximum control, no-code embedded components for speed, and a white-label portal for platforms that launch with minimal engineering lift. Query APIs for transaction data and webhooks for near-real-time event notifications are baseline requirements for any production-grade integration. The result: faster integration, less engineering overhead, more time building the core product.

Vertical-specific payments customization

Generic payment infrastructure is not built for how vertical SaaS platforms operate. A construction platform handling progress billing has different requirements than a property management platform that collects HOA dues. The ideal provider offers support for compliant surcharge and service fee pricing for regulated industries, bulk sub-merchant onboarding, and Level II and Level III data submission for interchange optimization on B2B card transactions.

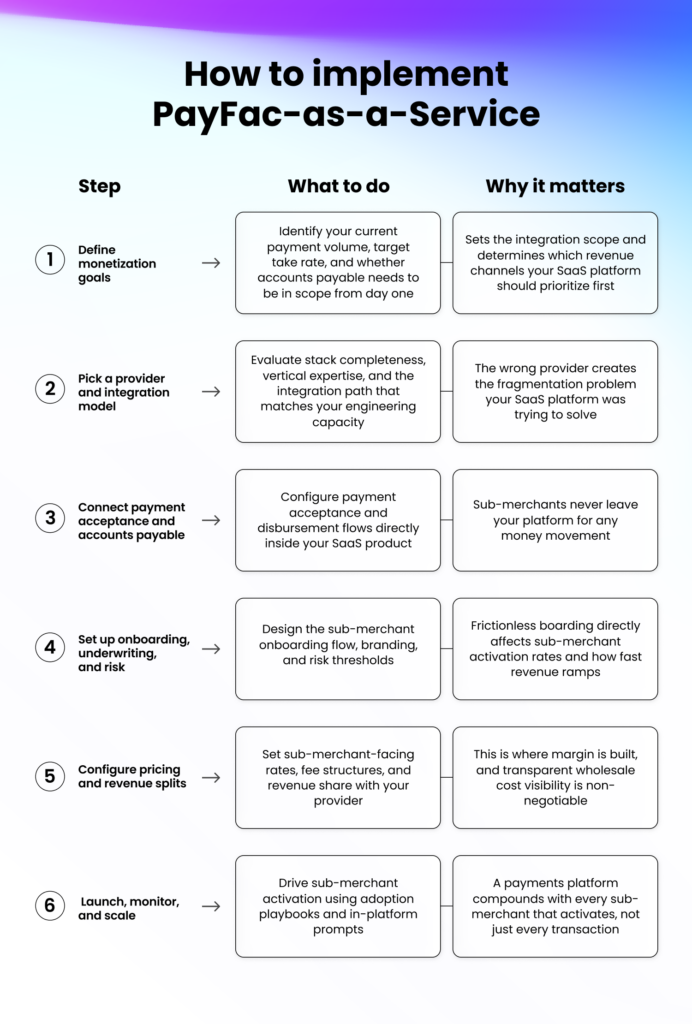

How do I make PayFac-as-a-Service work for my SaaS platform?

Getting from the decision-making phase to live transactions is straightforward when the sequence is right. Here is how vertical SaaS platforms implement PayFac-as-a-Service:

What does PayFac-as-a-Service look like in practice?

The best way to understand what PayFac-as-a-Service delivers for vertical SaaS is to look at platforms that have already made the switch. The results speak for themselves.

How Builder Prime grew payment volume by 1,000%

Builder Prime is a CRM and project management platform built for home improvement contractors. Before Payabli, payments were handled through a third-party processor. Sub-merchants onboarded outside the platform, the experience was disconnected, and Builder Prime had no visibility into payment activity or margin on transactions.

After embedding payment acceptance directly into its platform through Payabli, sub-merchants could accept cards, ACH, and checks inside the product they already used daily. The payment experience was white-labeled, the sub-merchant relationship stayed with Builder Prime, and the platform started earning on every transaction processed. Payment volume grew by 1,000% and embedded payments became a core retention driver, not just a processing utility.

Read the full Builder Prime case study.

How Sunbound scaled with embedded payments

Sunbound is a modern senior living finance platform. Before Payabli, payments ran through Stripe outside the core product, limiting pricing flexibility and leaving margin on every transaction with someone else.

Sunbound integrated with Payabli in under one month with a single developer and one project manager. Payment acceptance, sub-merchant onboarding, and reporting all moved inside the platform. The impact on sub-merchant activation was immediate: before Payabli, around 50% of payors used the payment flow. After embedding payments inside the platform, that number climbed to 90%.

Read the full Sunbound case study.

How Payabli powers PayFac-as-a-Service for SaaS

The right PayFac-as-a-Service partner gives your platform the economics, the sub-merchant experience, and the operational infrastructure to run a payments business without becoming one. Here is how Payabli delivers that for vertical SaaS.

One API for Pay In, Pay Out, and Pay Ops

Most platforms that try to build a payments business end up managing six or more vendor relationships. Payabli replaces that with one. A single unified API covers payment acceptance, accounts payable, and payment operations, so your team integrates once and owns the full payments experience from day one.

Built for vertical SaaS

Payabli powers over 70 vertical SaaS platforms across property management, field services, construction, education, and government. Customers, including Roofr, BuildOps, PayHOA, and Builder Prime, have turned payments into a core revenue stream without building the infrastructure themselves. See how Payabli works for SaaS companies.

Go live fast with hands-on support

Payabli partners have gone live in under a month with one developer and one project manager. A dedicated team is assigned from day one, not a ticketing queue, with support via email, Slack, and phone. Book a demo to see what the economics look like for your platform.