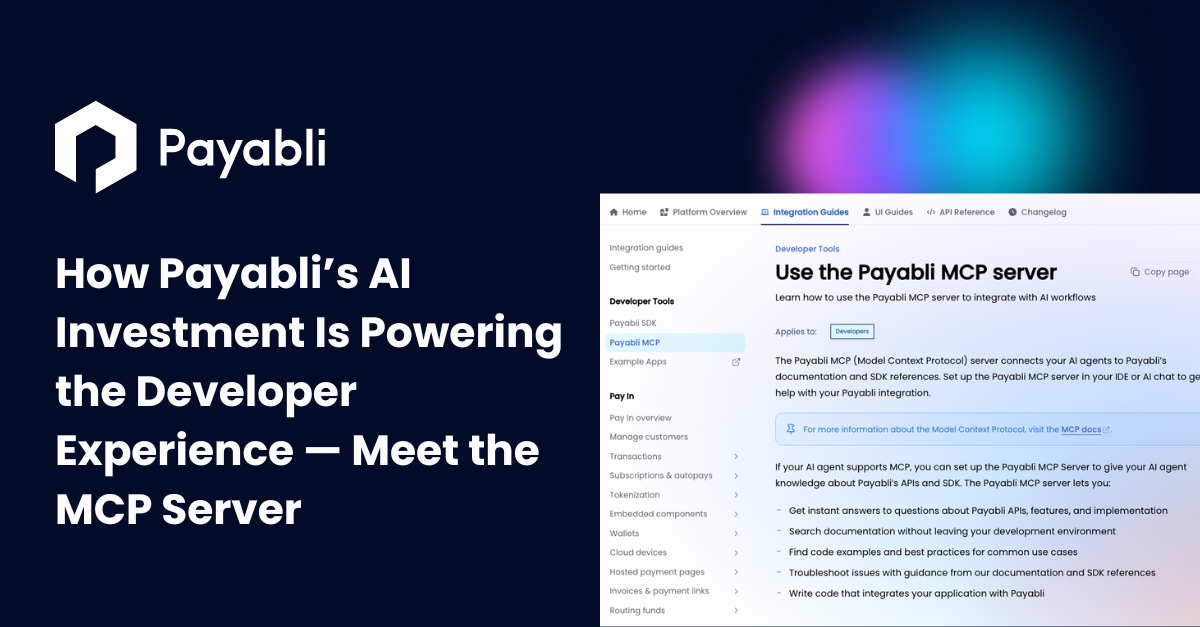

Your AI assistant’s payment expertise.

When we announced our $28M Series B funding, we shared our vision for the future of payments—one where AI plays a central role in how developers build and interact with payment infrastructure. Today, we’re bringing that vision to life with the launch of the Payabli MCP (Model Context Protocol) Server—the first of several AI-powered tools that mark the beginning of a new era in AI payment infrastructure and fundamentally change how developers integrate with our platform.

The Problem We Set Out to Solve

Every developer building with payments APIs faces the same frustrating workflow: code for a few minutes, switch to documentation, search for the right endpoint, copy code samples, switch back to the Integrated Development Environment (IDE), repeat. This constant context-switching kills productivity and slows down innovation.

We knew AI could solve this, but existing AI coding assistants lack the deep, real-time knowledge of payment systems that developers actually need. Generic responses don’t cut it when you’re handling sensitive financial data and complex compliance requirements.

AI Payment Infrastructure: Investment in Action

The Payabli MCP Server represents exactly the kind of AI innovation we promised investors and developers. Instead of building another chatbot or documentation search tool, we created something fundamentally different: a direct pathway between AI assistants and our live payment infrastructure.

We’re also early adopters of the Model Context Protocol (MCP) – an emerging standard for connecting AI assistants to external data sources. By staying ahead of this technology curve, we’re ensuring that developers on our platform get access to the most advanced, context-aware AI tools as they become available.

Here’s what makes it revolutionary:

- Real-Time Documentation Sync: Your AI assistant accesses the same live API references in the Payabli Docs – no outdated examples or deprecated methods.

- MCP-Powered Payment Intelligence: Your existing AI agents can leverage our MCP server to deliver precise, context-aware guidance about the Payabli API, including payment flows, compliance requirements, and more.

- Zero Context Loss: Developers never leave their IDE. The AI brings Payabli expertise directly into their development environment.

What Developers Are Building

Early adopters are already using MCP to accelerate development across various industries:

- Construction software platforms implementing contractor payment workflows

- Educational technology companies setting up subscription billing for course platforms

- Government software providers integrating secure payment processing for public services

- HOA management platforms building automated dues collection systems

- Field Services software processing mobile payments for service appointments

Why AI-Enabled Payment Infrastructure Matters for the Industry

In today’s fintech landscape, many companies are bolting on AI as an afterthought – typically in the form of customer service chatbots or surface-level analytics dashboards. But these limited implementations miss the bigger opportunity: rebuilding the developer experience from the ground up with AI at the core.

We’re pioneering a new category: AI-native payment infrastructure. Instead of simply making payments “AI-enabled,” we’re flipping the paradigm—making AI development payments-native. This approach deeply integrates payment capabilities into AI systems, opening up transformative possibilities for automation, personalization, and scale.

As early adopters of Model Context Protocol (MCP) – an emerging standard for connecting AI assistants to external data sources – we’re staying ahead of the curve. MCP ensures that developers working within our platform can seamlessly build intelligent, context-aware payment applications using the most advanced tools as they emerge.

By embracing these AI-first principles, we’re not just improving fintech infrastructure—we’re reshaping the future of how AI and payments work together.

The Developer Impact

What excites us most isn’t the technology – it’s what developers will build with it. When integration friction disappears, innovation accelerates. We’re already seeing:

- Faster time-to-market for payment features

- Reduced errors with AI-guided implementation

- Higher quality integrations with built-in best practices

- More experimentation with advanced payment capabilities

- Reduced technical debt from cleaner, AI-guided implementations

Getting Started

Already using Payabli? Try the MCP Server and start building with AI-powered integrations today.

New to Payabli? Book a demo to see our embedded payment infrastructure and AI-powered developer tools.

This is just the beginning of AI-powered development at Payabli. Stay tuned as we continue rolling out more AI-powered tools.