Within weeks of joining Payabli, several observations became abundantly clear: I joined an extremely innovative company, I worked alongside a world-class team, and I knew close to nothing about embedded payments.

Today, 18 months later, we are transitioning as a company from startup to scale-up. We are now post-Series B, process more than $6 billion in annual payments volume, doubled our team size to well over 100 people, and now partner with many leading SaaS platforms servicing over 60,000 merchants across industries such as healthcare, field services, government, and property management. In 2025 alone, we hit 400% year-over-year growth, while maintaining a focus on reliability while we also innovate.

I feel privileged to be part of this extraordinary journey and rapid growth. I’ve also learned there is no faster education in payments than scaling infrastructure to onboard tens of thousands of merchants and reliably process billions in annual volume.

Every Generation Finds the Previous One’s Friction Intolerable

To begin understanding embedded payments, how the ecosystem operates, and where we are heading, I find it helps to trace the industry back to its origins.

The first payment on record was a barley ration issued to a temple worker in ancient Uruk around 3100 BCE, inscribed on a clay tablet in proto-cuneiform script.

Five thousand years of innovation followed. Coins replaced barley. Paper currency replaced coins. Banks emerged to hold deposits and extend credit. Checks let merchants settle without carrying cash. Each step forward took centuries.

Then came the 1950s. Computing, telecommunications, and consumer finance converged, accelerating what had evolved gradually for millennia.

- 1950 – Diners Club launched the first universal credit card, extending trust at scale to strangers via “buy now, pay later.”

- 1958 – Bank of America introduced BankAmericard (the precursor to Visa), pioneering revolving credit lines for consumers.

- 1967 – The first ATM in London made banks accessible 24/7, diminishing the need for human tellers.

- 1970 – CHIPS enabled digital transfers of billions, digitizing institutional money long before consumers.

- 1997 – SMS purchased a Coke in Finland, turning phones into nascent wallets.

- 1998 – PayPal launched peer-to-peer transfers, simplifying cashless sharing.

- 2010 – 10,000 BTC bought two pizzas – a curiosity worth hundreds of millions today, igniting decentralized finance.

- 2014 – Apple Pay mainstreamed contactless payments, turning “tap to pay” from novelty to norm.

- 2020 – The COVID pandemic compressed a decade of digital adoption into months; cash became a liability, and adaptable payment stacks determined survival.

- 2024 – AI agents began autonomous purchases – booking flights, ordering supplies, and handling B2B deals. Legacy APIs, built for human clicks, now faced millisecond agentic commerce as an urgent engineering reality.

The pattern is hard to miss: every generation finds the previous one’s friction intolerable and invents something new. What once required clay tablets now happens in milliseconds. What once required bank branches now happens on your phone. Before each of these milestones, the very thought seemed impossible.

This is precisely what I love about Payabli; we are building the next generation of payments infrastructure that currently seems impossible, but will one day be written about.

Why Payments Architecture Cannot Be an Afterthought

Embedded payment infrastructure demands a different mindset than most software. In a typical application, a bug means a bad user experience. At Payabli, the stakes are higher. A single misstep in our systems can cascade into real-world consequences: an HVAC contractor unable to meet payroll, leaving technicians unpaid; a delayed utility disbursement plunging thousands of homes into darkness; a property management firm stalled on rent collections, threatening eviction timelines and tenant stability. These aren’t hypothetical edge cases, they are the lived realities of the merchants and communities who depend on us.

This unforgiving reality profoundly shapes every decision we make: how we architect systems with layered redundancy and fault tolerance, how we test with obsessive rigor across each service, how we deploy using zero-downtime strategies, and how we respond to incidents with urgency and ownership when the inevitable occurs.

Payabli’s architecture reflects this discipline in its design as a single, unified platform – seamlessly integrating Pay In (payment acceptance), Pay Out (disbursements and payables), and Pay Ops (onboarding, risk management, billing, reconciliation, and reporting). While fragmented providers introduce brittle integrations and mounting risk as scale increases, our cohesive, developer-first API eliminates those weak points entirely, enabling software platforms to embed complete lifecycle control with both confidence and resilience.

The truth I’ve learned about payments engineering is that reliability and security are the product. A beautiful interface means nothing if the charge fails. A clever feature means nothing if settlement is delayed. Merchants don’t notice when payments work, they notice when they don’t. Our job is to be invisible.

People Matter More Than Architecture

Here’s something I didn’t learn in a computer science course: the best infrastructure is built by teams that truly enjoy working together.

I am grateful to work on such an incredible team. These are some of the most genuine, curious, intelligent, and hard working people I have ever met. We are largely distributed around the world, from New York City, to Casablanca, Dubai, and even Montevideo – yet this has not inhibited us in the slightest from building world class products together.

We trust each other to ship fast, flag problems early, and pick up the phone at odd hours without a second thought. This is largely a tribute to our leadership and those who built a foundation for us to build upon.

The Future: Humans and AI in Harmony

For centuries, humans were the bottleneck in payments – swiping cards, approving transfers, reconciling invoices. Every transaction relied upon human action.

That landscape is rapidly changing. Today, AI agents are executing autonomous purchases in production: booking travel, replenishing inventory, and settling B2B invoices; all in milliseconds, without checkout pages or human clicks. Legacy APIs, designed for deliberate human interaction, are now being stress-tested by relentless, agentic commerce.

While this is fascinating, full autonomy is not our destination. In high-stakes domains like healthcare, government, and property management, human intuition, oversight, and accountability will always be irreplaceable. The leaders in embedded payments will embrace both realities: empowering humans with seamless, intuitive tools while engineering robust infrastructure for the rise of AI agents.

With our Series B momentum, we’re building agentic AI applications with a problem-first approach, accelerating capabilities that solve real payment challenges, including:

- Amigo: Our embeddable AI agent that guides onboarding, resolves support queries, and surfaces real-time analytics.

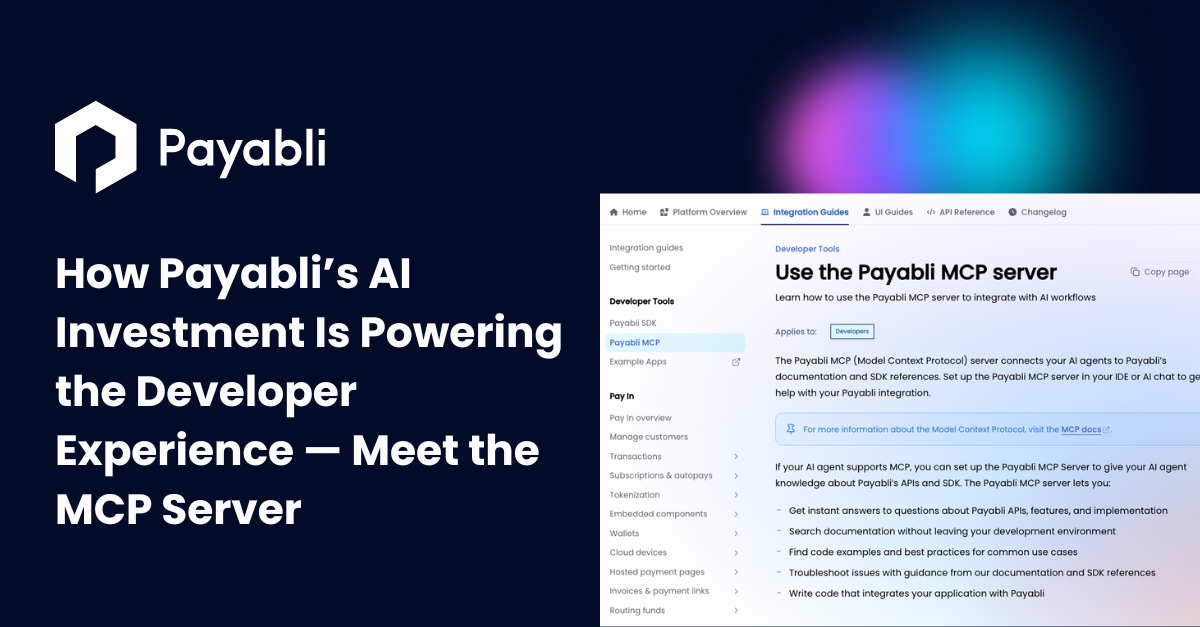

- MCP Servers: Secure bridges that connect external AI assistants to live payments infrastructure and documentation.

- Proprietary fraud models: Machine learning systems honed on deep, industry-specific data for tailored risk detection.

The winning platforms will not remove humans from the loop, they will make them superhuman. We are not awaiting the agentic future at Payabli; we are building it.