Commerce has evolved over millennia, and today, online businesses depend on electronic transactions to drive their operations. Customers expect the convenience of instant payments, which, while seeming magical, rely on complex systems behind the scenes. This article will explain what payment rails are, why they are important, and how they work to move money securely.

What Are Payment Rails?

Let’s start from the beginning – what exactly are payment rails? As the name implies, payment rails are similar to the physical rails that trains run on to transport goods over land. But instead of carrying physical items, payment rails transport money and data. Payment rails are the infrastructure and technology platforms that enable the movement of funds between payer and payee, facilitating transactions in the financial ecosystem. Think of them as the “tracks” on which payment information travels, similar to how physical railroads move goods and people.

These exchanges can happen between banks, businesses, and individuals. As such, they have become a crucial component of the financial ecosystem.

A Brief History of Payment Rails (1950-2010s)

You could argue that payment rails started with the first checks. These paper documents were like early versions of electronic payments and allowed customers to pay merchants without having the legal tender on hand. But it wasn’t until computers and electronic networks came along that payment rails took off.

In 1958, Bank of America introduced the first general-purpose credit card, the “BankAmericard,” marking the start of “card rails” and shifting payments from cash and checks to a credit-based system. This innovation evolved when BankAmericard became Visa in 1976, creating a global network that enabled cross-border payments and connected millions of merchants and cardholders.

About ten years after the launch of the BankAmericard, Automatic Clearing Houses (ACH) were introduced. ACH was developed as a solution to the growing need for efficient processing of large volumes of paper checks and electronic payments. The ACH network provided a way to move money between bank accounts electronically, facilitating transactions like direct deposit of payroll and automatic bill payments.

In 1978, SWIFT (Society for Worldwide Interbank Financial Telecommunication) revolutionized international finance by providing a standardized, secure messaging system for cross-border transactions. Before SWIFT, international payments were slow, costly, and error-prone due to the lack of a common protocol.

Then came the Internet, which completely transformed the payments landscape once again. The rise of the Internet in the late 1990s and early 2000s led to the emergence of Peer-to-Peer (P2P) networks, with PayPal being one of the most prominent examples. PayPal allows people to send and receive money digitally, bypassing traditional banks and payment methods.

Even traditional payment methods like checks have adapted to the digital age. With the advent of mobile banking, checks have received a modern update through mobile deposit features. Now, instead of visiting a bank or ATM to deposit a check, people can simply snap a photo of it with their smartphone and deposit it from anywhere.

In recent years, the development of real-time payments (RTP) has been a significant milestone in the U.S. payments landscape. Launched in 2017 by The Clearing House, RTP enables instantaneous transfers of funds between bank accounts, 24/7/365. Unlike traditional payment methods that could take days to process, RTP allows recipients to access funds immediately, even on weekends and holidays.

New payment technologies continue to evolve, with innovations like blockchain, digital wallets, contactless payments, biometric authentication, and AI pushing the boundaries of what’s possible. These advancements make transactions faster, safer, and more seamless, as the payments industry adapts to growing consumer expectations and technological capabilities in a digital-first world.

How Payment Rails Work

Payments can be categorized as push, pull, or a combination of both. Push payments offer control and are ideal for instant transfers, while pull payments are convenient for recurring bills and purchases. Systems like ACH provide versatile solutions for various business and personal finance needs.

- Push Payments: In a push payment, the payer initiates the transaction by sending money directly to the recipient. A great example of this is Real-Time Payments (RTP). With RTP, the payer actively “pushes” funds from their bank account to the recipient’s account. This type of payment is usually instant, and the recipient has immediate access to the funds, even on weekends or holidays.

- Pull Payments: On the other hand, pull payments work the opposite way. Here, the recipient or merchant initiates the transaction by requesting funds from the payer’s account. Credit cards are a common example of pull payments. When you make a purchase with a credit card, the merchant requests the amount owed from your credit card issuer, which then pulls the funds from your line of credit to pay the merchant.

- Combination of Push and Pull: Some payment systems can operate as either a push or pull, or even a combination of both, depending on how they’re used. ACH (Automated Clearing House) is a great example of this flexibility. ACH can function as a push payment when you, for instance, initiate a direct deposit to pay your employees—sending money from your account to theirs. It can also work as a pull payment when a utility company automatically withdraws your bill payment from your account each month.

The Formula for Processing Payments

While different payment rails might use slightly different methods, most follow a similar process. Here are the main steps:

- Initiation: The payment process starts when the payer authorizes the transfer of funds. That could mean swiping a debit card, signing a check, initiating a recurring payment, or logging into an online bank account and entering payment details.

- Payment Creation: Once the payer approves the payment, a financial message with relevant transaction data is generated. It includes the amount to be paid, account numbers, and other information required to complete the transfer.

- Processing: The payment message enters the payment network, which could be a card network like Visa or Mastercard or an ACH network. Here, a series of steps and checks ensure the transaction is valid and authorized.

- Confirmation: This step occurs as soon as funds are guaranteed and the transaction is authorized. Confirmation messages are returned to the payer, payee, and other relevant parties, serving as proof that the payment went through.

- Settlement & Reconciliation: Finally, the actual transfer of money occurs. This settlement process can happen instantly or not, depending on the type of payment rail. Once settled, accounts are reconciled and updated accordingly.

Types of Payment Rails

Now that we know what payment rails are, let’s look at the different types. We can group payment rails based on how they handle transactions, how fast they work, or what technology they use. Here are some of the leading payment rail systems in use today:

Automatic Clearing Houses (ACH)

ACH is a system that processes electronic payments in batches. It’s mainly used for direct paycheck deposits and automatic bill payments. In the US, ACH is overseen by NACHA (National Automated Clearing House Association).

One of the great things about ACH is that it’s affordable and perfect for recurring payments. If your paycheck gets deposited straight into your bank account every month, that’s probably through ACH. If you’re in the SaaS business and deal with ACH, check out our blog to learn more about ACH and ACH returns, how they work, and why they’re important.

Card Networks

Card networks like Visa, Mastercard, American Express, and Discover manage the infrastructure for secure and efficient card transactions. The process starts when a purchase is initiated, with transaction data sent through the network connecting the merchant’s bank (acquirer) and the cardholder’s bank (issuer). The issuer authorizes the transaction, verifying funds or credit, and once approved, the transaction is processed, transferring funds from the cardholder’s account to the merchant’s account.

Card Acceptance

Merchants can accept credit and debit cards as payment for invoices, goods, and services, expanding their customer base and streamlining their payment processes. Card payments can be processed online, by mail, over the phone, or using a physical point-of-sale device. Card details can also be stored for recurring payments, ensuring seamless transactions for subscription-based services or repeat purchases.

Additionally, merchants can leverage digital wallets to facilitate card payments, enhancing convenience for customers. Digital wallets enhance the security of card transactions by tokenizing and protecting card information. When a card is stored in a wallet, it is converted into a temporary virtual card at the time of purchase. This tokenization process ensures that the actual card details are never exposed during the transaction, reducing the risk of fraud.

Card Issuance

Card issuance allows individuals to obtain cards for making payments in person, online, or via mail/telephone orders. These cards come in various forms—credit, debit, prepaid, and gift cards—each serving different financial needs. Issued cards can be either virtual or physical, offering flexibility in how they are used. Additionally, cardholders benefit from purchase protection features, such as the ability to dispute unauthorized transactions, ensuring a fair and secure payment experience.

Interac

Since 1984, Interac has been Canada’s predominant payment network, linking financial institutions to process debit card payments at point-of-sale terminals and online. It also enables peer-to-peer money transfers through Interac e-Transfer, allowing account holders to send money using only an email address or mobile number, with SMS payments becoming particularly popular.

Domestic Wires

Domestic wires are a type of payment rail used to transfer money quickly and securely, typically for large-ticket items or transactions within a country. These transfers are instantaneous, making them ideal for situations where speed is crucial, such as high-value purchases or urgent payments. By leveraging established financial networks, domestic wires ensure that funds move efficiently between accounts, providing a reliable option for significant financial transactions.

Real-Time Payments and FedNow

This system, introduced by The Clearing House in 2017, revolutionizes payment processing by enabling real-time transactions with immediate fund availability, even on weekends and holidays. When a payer initiates a transaction through their bank’s online platform or app, funds are instantly transferred via the RTP network, allowing the recipient immediate access. Unlike traditional methods, RTP transactions are final and irrevocable, providing instant confirmation to both parties.

RTP Push and Requests for Payment

RTPs are initiated as a “push” of funds, meaning the payer actively sends money to the recipient, with no way to directly “pull” or debit funds from a payer’s account. Instead, businesses use a “Request for Payment” (RFP), which the payer must approve to process the payment. This method enhances security by ensuring payments require the payer’s explicit consent. RTPs provide instant access to funds, even on weekends.

FedNow

FedNow, an upcoming real-time payment service from the Federal Reserve, aims to enable instant transactions between banks 24/7/365. It will expand real-time payment access across the financial system, especially for smaller banks and credit unions, enhancing speed, efficiency, and accessibility for U.S. payments.

Payment Rails for SaaS Platforms

At Payabli, we like to say, “If you’re a software company, you’re a payment company.”

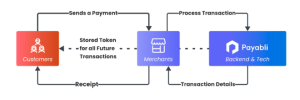

Every business, including SaaS companies, must handle payments and manage their entire lifecycle, from initiation to settlement. This includes processing sales, subscriptions, and paying bills for services like internet and vendors. By allowing users to manage these inflows and outflows in one place, you empower them to grow their business efficiently through your platform. Partnering with Payabli offers secure, fast, and convenient tools to support this growth. Here are some benefits:

Compliance & Security

In fintech and banking, navigating financial regulations and data security standards can be complex. Payment rails streamline compliance by transmitting payments through regulated networks that adhere to strict standards. Payabli complies with PCI Security Standards to ensure cardholder data is protected and NACHA standards to safeguard ACH transactions. This ensures that all sensitive payments are securely handled and compliant with all relevant regulations.

Speed

Payments once took weeks, causing delays and frustration. Now, payment rails enable transfers within hours or minutes. Time-sensitive SaaS companies benefit from faster settlements, improving cash flow visibility and decision-making. APIs offer instant payment requests, eliminating the wait for paper checks, while real-time status updates provide near-instant notifications when payments are funded or paid.

Customer Experience

The modern consumer and business expect fast, convenient online payment experiences with multiple options, from cards to mobile wallets. Payment rails help SaaS platforms meet these expectations by enabling payments through credit cards, debit cards, ACH transfers, and mobile wallets like Apple Pay or Google Pay. They also allow for easy payment processing via hosted payment pages or embedded checkout solutions. The result is improved customer satisfaction, loyalty, and increased referrals.

The Future of Payment Rails

Predicting the future of payment technology is challenging, but payment rails are likely to evolve in three key areas. First, payment rails change with technology; the rise of the Internet brought systems like PayPal and Stripe, and blockchain could lead to more decentralized rails. Second, AI can enhance payment processing by improving fraud detection and making transactions safer. Lastly, payment rails will increasingly integrate with other services like accounting, billing, and identity verification, creating a more holistic financial experience.

Get Started With Payabli

If you’re running a SaaS or platform business, the time is now to integrate compliant payment capabilities that help you scale globally. If you don’t, you risk falling behind your competitors.

Payabli offers the next-generation payments infrastructure to help software companies quickly embed world-class payments into their platform. We cover all aspects of payments: Pay In, Pay Out, and Pay Ops (we call these the 3Ps).

Book a demo with Payabli today to see how you can enable fast, secure payment acceptance through global payment rails with just a few lines of code.