Key takeaways

SaaS payment processing moves a customer’s money into your software customer’s account through a chain of banks and networks, each taking a fee along the way. That margin exists whether or not your platform captures it.

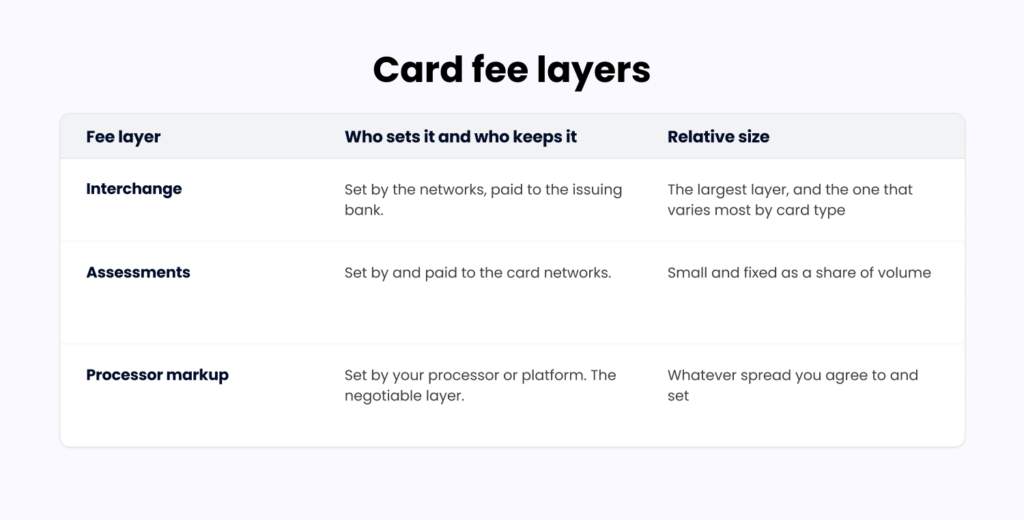

Interchange goes to the cardholder’s bank, and assessments to Visa or Mastercard. Neither is negotiable. The only layer that moves is the processor markup, which is exactly what a blended flat rate hides from you.

You generate revenue by pricing software customers above wholesale cost and keeping the difference, then splitting that spread with your infrastructure provider. It rides on volume already flowing through your product, so it grows as your software customers grow, with no new customers to sign.

Your model (referral, registered PayFac, or PayFac-as-a-Service) sets how much control, revenue, compliance, and liability you carry. Most vertical SaaS platforms take the full economics without the registration, through PayFac-as-a-Service.

Every SaaS platform that touches money is already a payments business, but most aren’t earning like one. SaaS payment processing is the machinery that carries a customer’s payment from their card into your software customer’s account, and every party in that chain takes a fee on the way through. Knowing who takes what is the difference between treating payments as a cost and treating them as revenue.

How does a payment actually get processed?

To the buyer, a card payment is a single tap, but behind it sit five or six parties, and the fee your software customer pays gets split among them before a cent reaches your platform. Understanding where your margin comes from starts with knowing who is in the room and what each one is paid to do.

Who are the players (and what each one takes)

The card networks call this the four-party model, though in software it usually runs to six, and each party has a distinct job that comes with its own price.

| Party | What they do | What they take |

| Cardholder | The customer is paying your software customer. | Nothing. They pay the sticker price. |

| Issuing bank | Issues the customer’s card and fronts the money. | Interchange is the largest slice of the fee. |

| Card network | Visa, Mastercard, Discover, or American Express routes the transaction. | Assessments, a small fixed cut of volume. |

| Acquirer/processor | Connects your software customer to the networks and moves funds. | A markup on top of interchange and assessments. |

| Payment facilitator | Holds the master account and onboards sub-merchants. | A share of the markup for owning risk and onboarding. |

| Your platform | Embeds payments in the product your software customer already uses. | The spread you set above the wholesale cost. |

Most of the fee never reaches your processor because it lands with the issuing bank as interchange and with the card network as assessments. That split shows you exactly which part of the cost is fixed and which part is yours to price.

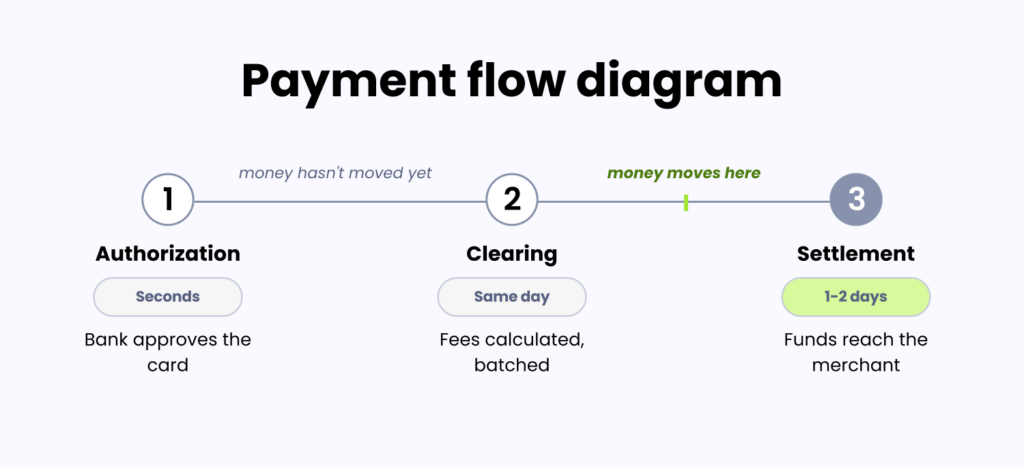

Authorization, clearing, and settlement

A card payment moves through three stages that do not happen at once: authorization clears in seconds, while settlement takes a day or two, and the gap between them is what decides when your software customer actually gets paid.

That same gap is also why fund holds happen, because on a shared-account aggregator model, your software customer’s money sits in a pooled account the platform does not control, so a single risk flag can freeze it with little warning. Owning the onboarding and the account relationship is what removes that failure mode.

What does processing actually cost?

Before you can price payments or judge a provider, you need to know what a transaction actually costs to run, and the largest portion of that cost comes from network and issuer fees that are set across the payments ecosystem.

Interchange, assessments, and processor markup

Every card fee breaks into three layers, whether the statement lists them separately or blends them into one rate.

Interchange is a schedule with hundreds of categories, and in places, the floor is set by regulation. Debit interchange for large issuers is federally capped under the Federal Reserve’s Regulation II, while credit carries no such cap, which is why a premium rewards card can cost several times more to accept than a debit tap on the same purchase.

Interchange is a schedule with hundreds of categories, and in places, the floor is set by regulation. Debit interchange for large issuers is federally capped under the Federal Reserve’s Regulation II, while credit carries no such cap, which is why a premium rewards card can cost several times more to accept than a debit tap on the same purchase.

Which fees can you negotiate?

Interchange and assessments are wholesale fees set by the card networks, not by processors, so processors cannot negotiate them down and simply pass them through. The markup is the only thing that moves, hence, a blended flat rate is worth a second look: folding all three layers into one percentage feels simpler, but it hides the markup completely, whereas interchange-plus pricing breaks it out as its own line so you can compare providers on the one number that actually differs.

There is also a lever on the interchange itself. Passing Level II and Level III data on B2B card transactions, details like tax amount and line items, qualifies those payments for lower interchange categories, and for platforms serving business customers, that is the real margin most overlook.

How do SaaS platforms make money on payments?

Payments become revenue at exactly one point in the chain: the markup. How much you keep comes down to how you price and structure it.

Setting customer pricing

The gap between wholesale cost and what your software customer pays to accept a transaction is where your platform earns. Once you set the customer rate and subtract interchange, assessments, and your provider’s cost, whatever’s left is yours.

Revenue share with your infrastructure provider

You rarely touch sponsor banks or card networks directly. Your infrastructure provider secures the wholesale rates and passes them through, leaving you to price software customers on top and keep the spread. The fewer intermediaries taking a cut along the way, the more margin reaches your platform.

How does economics compound with volume?

Subscription revenue grows only when you add customers, whereas payment revenue grows every time your existing software customers process more transactions. With no upsell and no new contract, it has become the larger line for so many platforms. Payment revenue through US software vendors has been growing around 20% a year and shifting toward the platforms embedded in customer workflows, and the guide on how to monetize payments maps where that revenue sits in detail.

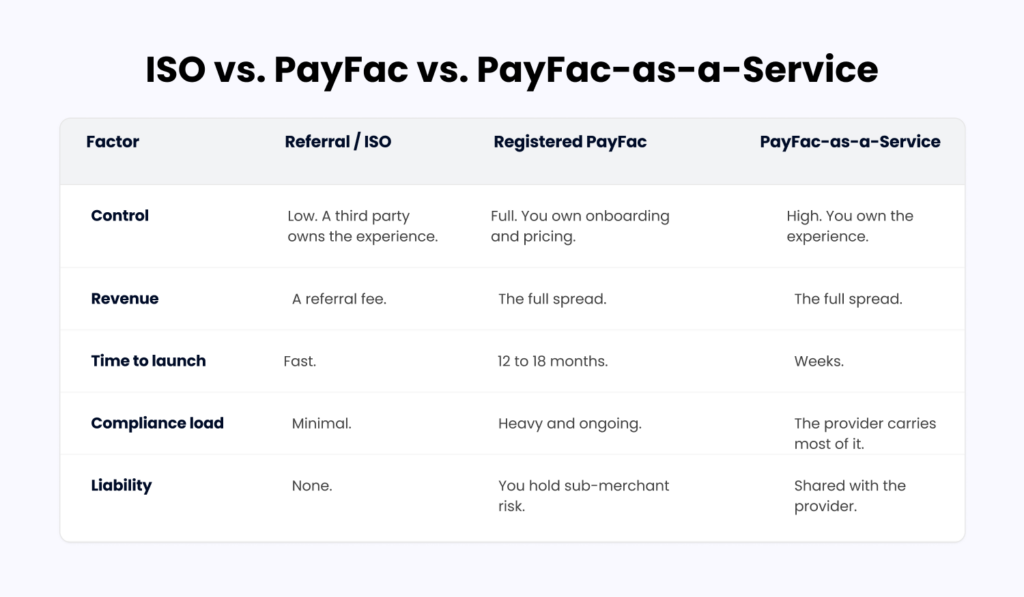

ISO vs. PayFac vs. PayFac-as-a-service

There are three ways to structure a payments business, and they trade control against effort, so the choice comes down to how much of the machine you actually want to own.

Referral / ISO

Referral / ISO

Referring software customers to a processor makes sense only when payments are incidental to your product, because it hands away pricing, data, and nearly all the margin on volume you generate.

Becoming a payment facilitator

Full registration only makes sense at a serious scale, and even then, the spread on your volume has to clear the cost of the capital, the sponsor bank relationship, and a compliance team you have to staff and keep staffed. For most platforms, that cost outweighs the control it buys.

PayFac-as-a-service

For most vertical SaaS platforms, PayFac-as-a-Service is the default, since it delivers the same economics as full registration without the multi-year build. If you are weighing registration against it, these payment facilitator myths are worth reading first.

What do you have to handle: compliance and risk?

Owning payments means owning some responsibility for them, and while none of it should keep you out, you should know which parts land on your team and which a provider absorbs.

PCI compliance

Any platform that touches card data falls under the PCI Data Security Standard, where the real question is scope, because routing raw card data through your own servers pulls you into a heavy audit, whereas a provider whose tokenization and embedded components keep that data off your systems shrinks the obligation to a short self-assessment without erasing it.

Customer onboarding and underwriting

Before a software customer can process, someone has to verify the business and price its risk through KYB checks, a look at the business model, and often tighter limits or reserves for newer accounts. While PayFac-as-a-Service providers hand that underwriting to the provider, you feel the benefit in activation speed, which is why a provider tuned to your vertical beats a generic one.

Chargebacks and fraud

A chargeback is a customer disputing a charge through their bank rather than asking the software customer for a refund, and whoever holds sub-merchant risk eats the loss when it cannot be defended, so keeping dispute ratios low is the monitoring discipline that card networks watch closely and that payment operations tooling exists to handle.

Build vs. buy: should you process payments yourself?

This is really a question about focus, since the capability is buildable, but consider whether it is worth pulling engineers off your core product to do it.

What building in-house actually requires

Building the full stack means securing sponsor bank relationships and standing up a gateway, tokenization, an underwriting engine, reserve and funding logic, dispute workflows, reconciliation, and reporting, then keeping every piece compliant as the rules shift, which adds up to running a payments company inside your software company and fighting your own roadmap for engineers.

What infrastructure carries for you

The alternative is one integration that carries the plumbing, where a unified API spanning payment acceptance, accounts payable, and payment operations lets you integrate once and own the experience while the provider runs onboarding, risk, compliance, and settlement behind it, and no-code components get payments live for teams that want speed over engineering lift.

Add payments to your platform with Payabli

Payabli gives vertical SaaS platforms one API for Pay In, Pay Out, and Pay Ops, so you earn on both sides of money movement without the capital or compliance burden of full PayFac registration, and it already powers over 70 platforms across property management, field services, construction, education, and government.

The results show in the numbers: Builder Prime grew payment volume by 1,000% after embedding payments, and Sunbound scaled to over $1 billion in annual payments while cutting reconciliation workload in half.

Book a demo to see the economics for your vertical.

Frequently asked questions

What’s the difference between a payment processor and a payment facilitator? A processor moves the transaction between banks and networks, while a payment facilitator sits on top of one, holds the master merchant account, and onboards sub-merchants beneath it, owning the pricing, the relationship, and the risk the processor never touches.

How much can a SaaS platform earn from payments? It scales with your processing volume and the spread you keep, and since that revenue grows alongside your software customers, it compounds without new customer acquisition, so the right infrastructure partner can model the range for your vertical.

Do I still need to be PCI compliant if I use a payments provider? Yes, but far less onerously, since a provider that keeps raw card data off your systems through tokenization and hosted fields cuts the obligation to a short self-assessment instead of a full audit.

How long does it take to add payments to my software? Usually, weeks with PayFac-as-a-Service, against the 12 to 18 months a full registration demands, and some platforms go live in under a month using an API for control or no-code components for speed.