Key takeaways

- A financial account gives merchants real accounts, routing numbers, FDIC-insured deposits, ACH, a debit card, and interest, all inside your platform. It turns a processing relationship into the merchant’s operating bank, and you never become one yourself.

- A chartered partner bank, sometimes reached through a BaaS provider, holds the deposits and carries the compliance. You own the distribution, the experience, and the integration.

- FBO accounts launch faster but limit functionality and muddy FDIC pass-through. Real individual accounts cost more to run but give each merchant clean coverage and full banking.

- Net interest margin is the main revenue: a 1.5 to 2 percent share of deposits today, about 1.5 to 2 million dollars a year on 100 million held, plus ACH, wire, and card fees. It moves with interest rates.

- Deposit insurance covers 250,000 dollars per depositor per bank; sweep programs across banks extend it into the millions. Merchants ask about this now.

- Accounts are the hub: lending, spend management, and Pay Out all work better once the money lives there.

Most payment platforms already show merchants a balance: the money they have earned but not yet swept to their external bank. It is useful, but it is only a ledger entry. A financial account is the real thing, with account and routing numbers a merchant can hand out, deposits that arrive from anywhere, ACH and wires going out, and often a debit card and interest on the balance. The banking a merchant used to do at a separate bank now lives inside the platform they already run payments on, and that shift changes what the platform is to the merchant.

What is a financial account?

A financial account is a bank-like account issued to a merchant, with real account and routing numbers, the ability to receive ACH and wire deposits, the ability to originate ACH and wire payments, and optionally a debit card, check-writing, and interest on balances. The merchant treats it as their bank account, while the money sits either at a partner bank or in a segregated pool inside a platform-controlled structure. Because the platform issues the account as a feature, the merchant never leaves the platform to bank, and the platform’s other products work against that same account, so payments, lending, and spend management all draw on one balance instead of scattering across tools. That native integration is what makes the account embedded rather than a separate bank sitting beside the software.

Banks are heavily regulated, and no platform can be one without a charter that almost none should pursue. The workable path is partnership, where a chartered bank carries the deposits, provides compliance, and runs core banking, while the platform provides distribution, the merchant experience, and the embedded integration.

How does it differ from a platform balance?

A platform balance is an internal ledger entry for funds a merchant has earned but not yet swept out, and it has no account number anyone can pay into. A financial account carries real, external-facing banking identifiers, so the merchant can take deposits from a customer or vendor, mobile-deposit a check, and originate payments to payroll or suppliers, with the platform’s infrastructure running the banking underneath.

What do merchants get from a financial account?

Consolidation is the main pull, and a handful of things make a platform account worth more than the bank a merchant already keeps.

Consolidation

A small business typically runs a bank, a processor, a payroll provider, a bookkeeping tool, a bill-pay service, and maybe a lender, so folding several of those into one platform cuts tools and hands back hours every month.

Speed and automation

Processing proceeds land in the account immediately rather than waiting to settle with an outside bank, and outgoing payments can fire on platform signals, so a merchant can pay vendors straight out of the day’s sales.

Integration depth

Because the platform can see the account, it can categorize and reconcile against processing automatically, manage cash flow, and lend against the balance, which a generic bank has no way to do.

Yield

Most platform accounts pay 2 to 4 percent on balances, well above the near-zero that most small-business operating accounts earn at traditional banks.

Building trust

Merchants are wary of moving primary banking onto a platform, so most begin with a supplemental account that holds processing proceeds and widen it as their confidence grows.

What financial accounts do for the platform

For the platform, a financial account changes two things at once: the revenue it earns from a merchant and how tightly that merchant is bound to the platform.

Deposit economics

Deposits earn net interest margin, the spread the bank makes between what it pays depositors and what it earns lending or investing those deposits, and the bank passes part of that spread to the platform.

Retention

A merchant whose money moves through a platform account rarely leaves, because switching means rebuilding banking elsewhere, and churn for account-attached merchants tends to run 3 to 5 times lower than for processing-only merchants.

A surface for other products

Lending underwriting sharpens once the platform sees total cash flow, spend cards fund straight from the balance, and Pay Out speeds up because the money already sits in the account.

Data

Every account tells the platform what a merchant pays, who they pay, and how much they hold, which is information that a processing relationship never surfaces, and it feeds underwriting and product decisions.

Valuation

Platforms with banking product lines tend to trade at higher multiples than pure SaaS or pure payments companies, and rational or not, that gap matters to investors.

FBO (For-Benefit-Of) accounts vs. real accounts

The accounts can be structured two ways, and the choice sets how fast a platform launches and how much banking merchants actually get.

FBO (For-Benefit-Of) accounts vs. real accounts

The accounts can be structured two ways, and the choice sets how fast a platform launches and how much banking merchants actually get.

| Dimension | FBO accounts | Real individual accounts |

| Structure | Platform holds master accounts at the bank; each merchant gets a sub-balance held for their benefit, tracked on an internal sub-ledger | Each merchant gets their own account at the partner bank, with their own account and routing numbers, and a direct (at least legal) banking relationship |

| Build and operate | Faster to build, simpler to regulate for the platform | More complex to build and operate |

| FDIC insurance | Less clear; pass-through must be set up carefully | Clean, per-merchant coverage |

| Functionality | Limited; the account number cannot always be used externally | Full banking functionality |

| Best fit | Launching fast; supplemental balances | Merchants using the account as their primary banking account |

Many platforms start FBO because it launches faster, then move to real individual accounts as the product matures; some stay FBO when the use case never needs full banking. Regulators have paid closer attention to FBO structures, especially when several intermediaries (platform, BaaS provider, bank) sit between a merchant and their money, so anyone building one has to be deliberate about how it is set up and how clearly FDIC insurance passes through to each merchant.

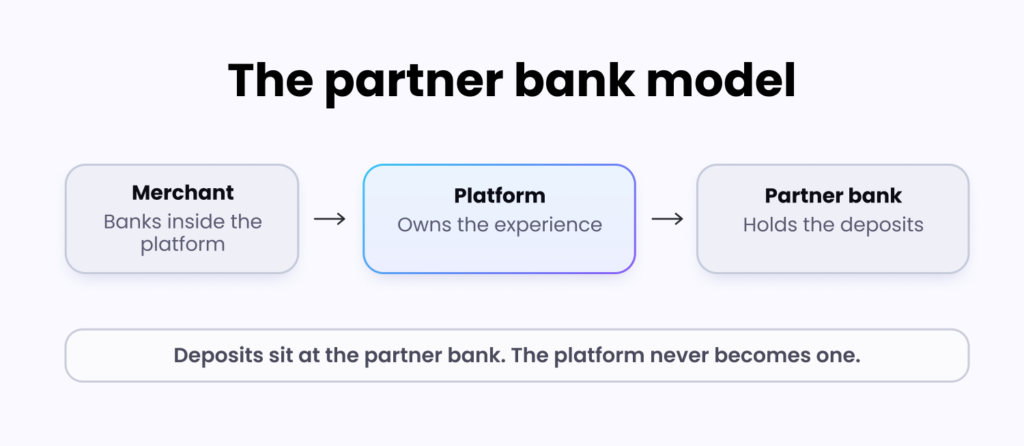

How does the partner bank model work?

Underneath every embedded account is a chartered bank doing the parts a platform cannot. The bank holds the deposits, provides the charter, FDIC insurance, and Federal Reserve access, runs core banking like settlement and interbank transfers, and sits for the regulatory exams. The platform owns what the merchant sees: distribution, the interface, the product design, and account-related support. Commercially, the platform pays the bank per-account and per-transaction fees, sometimes with minimum balances, and earns back a share of net interest margin plus pass-through transaction fees like ACH origination and wires.

The banks that do this are a narrow group, chosen on their track record with similar partners, technology readiness (modern APIs over a legacy core), operational flexibility, regulatory posture, terms, and balance-sheet stability. A platform in a hurry can instead go through a Banking-as-a-Service provider that bundles the technology and the bank relationship: faster to launch, but it takes a slice of the economics, which suits platforms that value speed over a direct bank relationship.

How do financial accounts make money?

Revenue comes from three places, and one dominates.

| Revenue stream | How it works | Typical economics |

| Net interest margin (NIM) | The bank earns a spread between what it pays depositors and what it earns lending or investing the deposits, then shares part of it with the platform | Primary stream. In a ~5% Fed funds environment, banks might realize 3 to 4% NIM and share 1.5 to 2%, about 1.5 to 2 million dollars a year on 100 million dollars of deposits |

| Transaction fees | ACH origination, wire, incoming wire, check services, and debit interchange are passed through to the platform | ACH 0.25 to 1.00 dollars each, wires 15 to 40 dollars each; adds roughly 10 to 30 bps of account volume a year |

| Account fees | Monthly fees (often waived above a balance minimum), overdraft fees, premium tiers | Secondary to NIM and transaction fees for most programs |

NIM tracks interest rates, which is the thing to understand about it. Through the zero-rate years from 2008 to 2022, it was a thin stream; in today’s higher-rate environment, it is substantial, which is why a platform launching a banking product now has far better economics than one that tried in 2015.

How does deposit insurance work for platform accounts?

Deposit insurance became a first-order merchant question after 2023, and a platform offering accounts has to answer it precisely.

The $250,000 limit

FDIC insurance covers 250,000 dollars per depositor, per bank, per ownership category, and anything above that at a single bank is uninsured if the bank fails.

Sweep programs

For merchants holding more, sweep programs spread the money across several partner banks, each carrying its own 250,000 dollars of coverage, which extends protection into the millions or tens of millions.

After Silicon Valley Bank

The 2023 SVB collapse made insurance a live concern for any business with real balances, and merchants now expect a clear answer on how much is covered, at which banks, and what happens to the rest if a partner bank fails.

FBO insurance

FBO structures hold up when pass-through is set so the FDIC recognizes each merchant’s sub-balance. Without that, coverage turns ambiguous exactly when it matters most, so the legal setup is what earns merchant trust.

What compliance and operations do financial accounts require?

Operating at the edge of banking carries banking’s compliance load, most of which the platform runs day to day, even though the partner bank holds ultimate responsibility.

- BSA and AML. The Bank Secrecy Act and Anti-Money Laundering rules bring customer identification, transaction monitoring, suspicious activity reporting, and OFAC screening.

- Customer due diligence. Know Your Business checks cover the merchant entity, and Know Your Customer checks cover the people behind it, with enhanced diligence and periodic refresh for higher-risk profiles.

- Regulation E. If the accounts reach consumers and not just businesses, Regulation E adds disclosures, dispute rights, and liability limits for unauthorized transactions, and that burden is significant.

- State licensing. Many states require money-transmission licenses for handling customer funds, even in an FBO structure, though some programs run under the partner bank’s charter to avoid platform-level licensing.

- Operations. Underneath it all sit fraud monitoring, dispute handling, customer service, and the account lifecycle from opening to closure, each a capability that costs money to build.

What treasury products do financial accounts unlock?

Once a merchant parks real balances in the account, adjacent products open up. Cash management adds yield through sweeps into interest-bearing accounts, laddered CDs, or money-market funds, and the platform shares in that yield. With visibility into balances and flow, the platform can offer working capital proactively, like an automatic draw against processing when an account that usually holds 50,000 dollars drops below 20,000 dollars. Accounts can fund payroll directly, cutting out the hop from operating bank to payroll provider to employees. Multi-currency accounts, FX conversion, and international wires matter for merchants with overseas customers or suppliers. Each of these makes the account stickier while the account makes each of them work better, so platforms that launch accounts tend to see lending uptake, card usage, and Pay Out volume rise together.

How Payabli supports financial accounts

An account changes what the platform is. It moves the merchant relationship from accepting payments to running financial operations, a far stickier place to sit, and it becomes the hub that makes lending, spend management, and payouts all work better. That is also why accounts are the closest thing to a moat in embedded finance: expensive to build and operationally heavy.

Payabli’s role is the connection points between payments and the account, across Pay In, Pay Out, and Pay Ops: settlement can land directly in a designated account, FBO or real; a merchant already processing with Payabli has cleared KYB, compliance, and sponsor-bank setup, so opening an account reuses that context; and risk signals from processing can drive account-level decisions like monitoring or holds. With a partner bank or a BaaS provider holding the account, the platform never has to become a bank, and building on Payabli now means no re-architecting when accounts become a priority.

Book a demo to talk through what financial accounts could look like on your platform.