Security in payment transactions is crucial for software businesses, and payment tokenization offers an innovative solution to this challenge. As we mentioned in our previous blog, there are multiple types of tokenization including standard, multi-use, and network tokenization. Each can benefit a software business’s unique use case and play a crucial role in its payment strategy.

In this blog we take a step back to explore the fundamentals of payment tokenization, why it matters for software businesses, its role in safeguarding sensitive payment data, and its impact on transaction security. We also emphasize the significance of partnering with the right payment provider for seamless and secure token migrations, ensuring a smooth experience for software businesses and their customers.

What is Payment Tokenization?

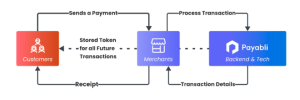

Payment tokenization involves replacing sensitive payment data, such as credit card numbers or bank account details, with randomly generated tokens. These tokens are used to facilitate secure transactions without exposing actual payment information. When a customer initiates a transaction, the payment system generates a token representing that information instead of transmitting their payment information, such as credit card or bank account details. This token is then passed through the payment process and stored in your business’s payment platform for future usage. If the token were intercepted, it would be rendered ineffective for use by unauthorized individuals or hackers, because it does not contain any sensitive data. The diagram below shows how payment tokens work for software businesses and their customers, and how the payment platforms’ backend tech, such as Payabli helps facilitate the payment tokenization process.

Why Does Payment Tokenization Matter for Software Business?

For software businesses, payment tokenization enhances security by reducing the risk of data breaches and fraud. It allows them to handle payment transactions without storing sensitive data, thus minimizing liability and compliance requirements. Additionally, payment tokenization enables software businesses to offer their customers a safer and more secure payment experience, which can enhance trust and loyalty.

Graph from EMV Co

Exploring Different Types of Payment Tokens

There are three generally well-known forms for tokens:

Traditional Payment Tokens: These tokens are generated by replacing sensitive payment card details such as credit card numbers with a randomly generated string of characters. Many PCI-certified gateways and processors have enabled this functionality for many years. Since they are managed by your payment service provider, they tend to be the easiest and cheapest method to manage recurring payments.

Device Tokens: Device tokens are associated with specific devices, such as smartphones or smartwatches, and are used in mobile payment systems like Apple Pay, Google Pay, or Samsung Pay. Instead of using the primary account number, the payment system generates a unique token tied to the device’s secure element or software.

Network Tokens: Unlike traditional tokens or device tokens, which are generated by merchants or payment processors, network tokens are created and managed by the card networks themselves. These tokens can be automatically updated since they are linked to the issuer and network if a change occurs.

Payment service providers like Payabli work with all three of these modalities to provide a convenient and secure payment processing experience for our software Partners.

That Seems Too Easy… What’s the Catch? And What Does This Mean For Software Businesses?

As mentioned above, traditional tokens are stored with either the gateway or processor. This means those platforms are managing the token lifecycle on behalf of customers and thus control the flow of that data. If a merchant or software provider (ISV) had to switch to a new gateway or processor, they would have to migrate all those saved tokens or even risk losing them all. Not having access to those tokens could have a massive impact on the merchant’s ability to process transactions and could affect their business operations overall.

There are two key factors that software platforms need in order to save their clients from this grief:

- Token Portability: When working with a provider that processes your payments, make sure you can migrate your tokens to a new provider.

- Token Migration: When you select a new payment service provider, it is important to ensure they can handle token migrations. Are they PCI-compliant and do they have a formal process to ingest the token information securely?

How does Payabli Do it Better?

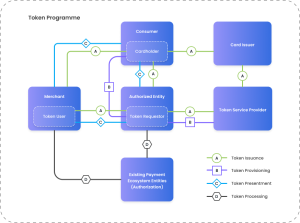

Migrating a token may sound simple but it tends to be fraught with error. At Payabli, our team of payment experts has spent a significant amount of time normalizing data from the largest players in the payments space to ensure that migrations work smoothly for software businesses. You can see in the diagram below how the token migration process works within our technology ecosystem.

Moreover, we have automated the process, which often takes 2-3 weeks with other payment providers, down to a one-day process.

Here’s how we help facilitate the token migration process in a timely and secure manner:

- We set secure file transfer protocol (SFTP) inboxes for our clients to deliver the information

- We have built proprietary tools to standardize the formats from big payment service providers in the industry

- We automatically decrypt the files and extract all the information

- We create Payabli tokens for our merchants to be able to process transactions immediately

Conclusion

In conclusion, payment tokenization stands as a cornerstone of modern transaction security for software businesses, providing a robust shield against data breaches and unauthorized access. By adopting this technology, businesses not only safeguard sensitive payment data but also enhance the trust and confidence of their customers. Partnering with the right payment provider, such as Payabli, further amplifies these benefits through efficient token migrations and management, ensuring that the payment process remains seamless and secure. Payabli not only simplifies compliance with PCI standards but also equips businesses with the tools necessary for handling complex token migrations effectively. Therefore, embracing payment tokenization is not just about adopting new technology—it’s about investing in the future of secure, reliable, and customer-centric digital transactions.

Interested in learning more? Our team of payment experts would love to chat. Schedule a demo here.