Key Takeaways

- Embedded finance works by incorporating financial services (embedded payments, Pay In, Pay Out, and Pay Ops) into the software that is already being used by a business.

- Embedded payments are not a synonym for embedded finance. Embedded payments fall under embedded finance alongside other financial services like card issuance, lending, working capital, banking-as-a-service (BaaS), and insurance.

- Partnership with a payments provider is the fastest path toward integrating embedded finance into your platform. Instead of building your own payment system, you can work with an infrastructure partner that already has the necessary licenses, banking relationships, and compliance machinery to save on time and valuable resources.

- Owning payments makes vertical SaaS stickier because it turns every transaction into a revenue opportunity.

- The global embedded finance market is expected to grow at a 33% CAGR until 2034, after hitting $145 billion in 2025. This makes embedded payments a must for organizations that want to stay competitive.

Despite being one of the most-used terms in the tech industry, often applied to almost everything from checkout buttons to full-blown lending programs, the true meaning of embedded finance continues to escape us. But what counts as embedded finance? And how can you make it work for a SaaS platform?

In this article, we will walk you through the definition of embedded finance, how money moves through it, who manages what, and how to incorporate it into your SaaS operations.

What is embedded finance?

Embedded finance integrates financial services into non-financial software, allowing people to make and receive payments, and borrow or manage money all in one place. It aims to bridge the gap between technology and financial systems, creating seamless transactions that do not require you to transfer to a separate environment to complete payments.

What falls under embedded finance?

It’s important to note that “embedded finance” is an umbrella term that encompasses an array of services, such as:

- Payments – receiving money from customers

- Payouts – sending money to vendors

- Lending and working capital – extending credit to merchants

- Card issuing – offering debit or credit cards

- Banking-as-a-Service (BaaS) and deposit accounts – funds storage

- Insurance – shielding merchants from risks like damage, liability, or loss of income

Bear in mind, each of these services is its own separate entity. They each come with licenses that need to be obtained, risks to be managed, and their own infrastructure requirements. Think of it this way: operationally, card issuance has nothing in common with underwriting a loan. This is why there’s no single provider capable of effectively handling all these services. And attempting to offer everything all at once can have major business consequences.

Luckily, most platforms don’t need the whole lineup. What you need to know is which of them your platform needs the most.

Embedded finance vs. embedded payments

Perhaps one of the most common misconceptions is that embedded finance is synonymous with embedded payments. Remember that embedded payments fall under embedded finance. Embedded payments enable platforms to own merchant relationships, pricing, payouts, and data, with ownership acting as the dividing line between these key aspects.

How does embedded finance work for SaaS?

In recent years, embedded payments have become the entry point for vertical SaaS platforms into embedded finance. Increasingly turning them into table stakes for organizations that want to own the experience of managing transactions on behalf of their merchants.

The quickest way to integrate embedded payments into your vertical SaaS platform is through a partnership. Instead of working your way into becoming a registered payment facilitator, which typically takes 12 to 18 months and requires substantial capital, you can team up with an infrastructure partner that is already equipped with the necessary licenses and capabilities. This way, your platform inherits regulatory and operational machinery instead of having to build it.

The partnership model is ideal for SaaS companies that are not and do not aspire to become financial institutions. But they are not the only organizations embedding financial services. Even banks and financial institutions are leveraging embedded payments to modernize their payment services. An example of this is Payabli’s partnership with Huntington Bank. Because of this move, Huntington’s digital banking experience can now ensure seamless transactions.

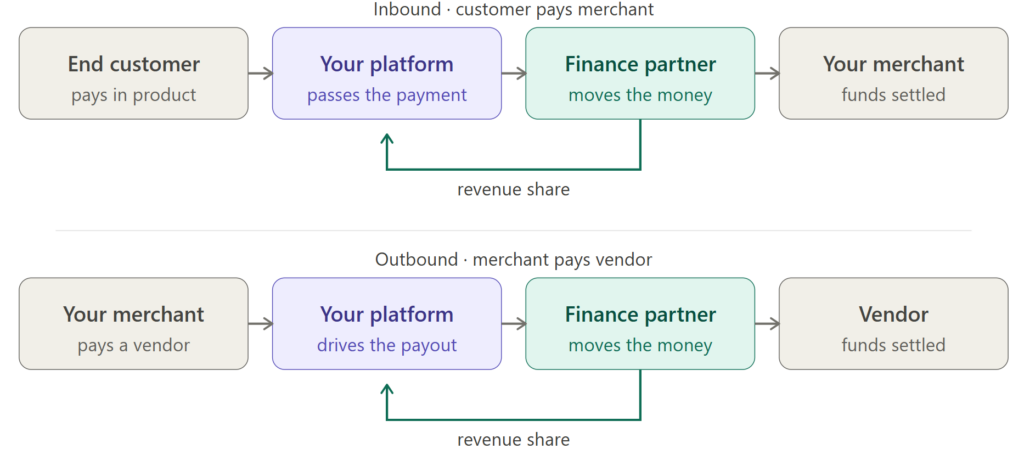

How does money flow through embedded payments?

Transactions are handed over to the infrastructure partner by the software whenever a customer makes a payment via a SaaS platform. It then passes through the partner’s processor and card network before transferring the appropriate funds into the merchant’s account and routing the platform’s share to its institution.

For example, a shopper purchases a pair of jeans from an online store that operates on an e-commerce platform. Instead of making their payment on a different site, the customer can complete the transaction from within the online store by simply entering their payment details at checkout. The platform then passes the transaction to its infrastructure partner, which is responsible for running the payment through card networks (Visa, Mastercard, etc.), validating it, and depositing it into the store owner’s account. A tiny portion of that transaction will also be sent to the e-commerce platform. The sale experience happens in a single place, while the e-Commerce service earns from every transaction.

Likewise, outbound flows happen in pretty much the same way except in reverse. The payment process is started within the e-Commerce platform by the store owner whenever they need to pay a supplier. The infrastructure partner will then route the funds and the platform’s share to the supplier and the service provider, respectively.

The bottom line: you can earn revenue every time money moves through your software, whether it be inbound or outbound.

Ownership matrix: Who owns what?

The table below outlines how responsibilities are divided between a vertical SaaS platform and its embedded payments partner:

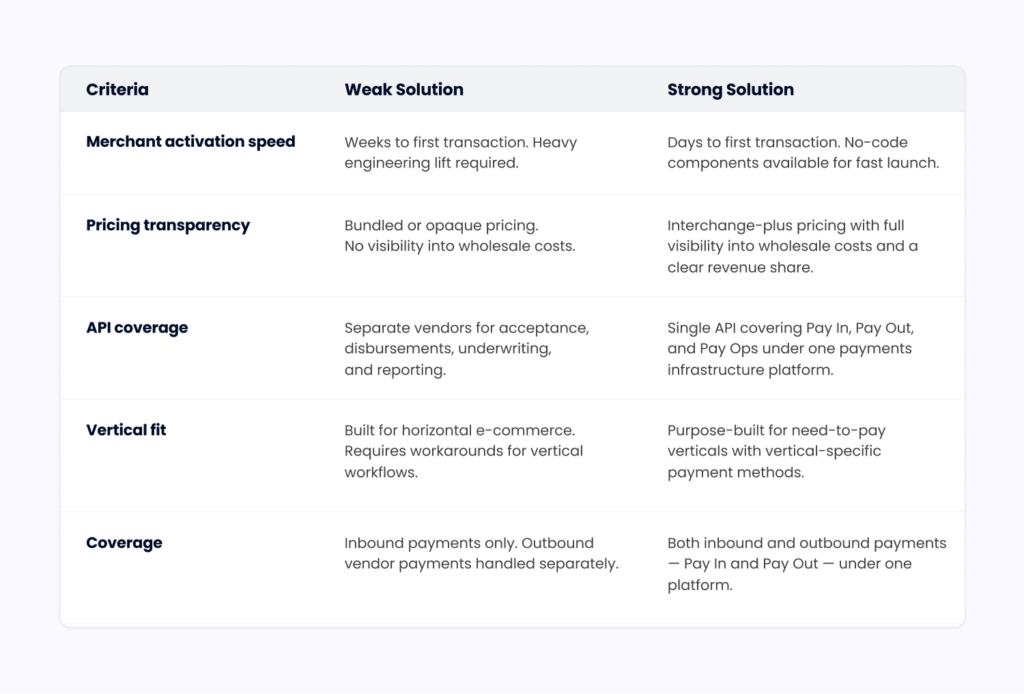

How long does implementation take?

Assuming that you will team up with a payments partner that already has the relevant licenses, implementation should only take a few weeks. According to Mastercard’s 2025 white paper on The future of payment facilitation, PayFac-as-a-Service models have collapsed time-to-market from months to weeks. This is especially important to vertical SaaS platforms because they need to be able to embed payments with one integration model built for speed.

Why embedded payments matter for vertical SaaS

It’s no secret that embedded finance can help cultivate the relationship between a platform and its customers. Let’s dive into the benefits of combining embedded payments with vertical SaaS:

-

Every transaction becomes a revenue opportunity

Without embedded payments, the processing fees on a platform’s merchant volume flow to a third party. With embedded payments, that margin goes back to the platform. Therefore, a platform of $100 million in annual volume at 1% generates $1 million in revenue, all without needing new customers.

-

Merchants are harder to churn

The payment experience should also take merchants into consideration. A merchant who collects, reconciles, and pays vendors inside a platform does not switch over a feature comparison. 64% of marketplaces were able to cut merchant churn by embedding payments into their platforms. Payments, when effectively facilitated, are the stickiest thing a vertical SaaS platform can own.

-

Revenue compounds better than subscription pricing

Subscription revenue grows when a platform signs new customers. In a study conducted by Andreessen Horowitz, on-premise payments can boost revenue by two to five times more than subscription models. Payment revenue grows when existing merchants grow their own businesses. The more your merchants sell and expand their operations, the more your platform will earn automatically. You won’t need new sign-ups or contracts for your revenue flow to increase.

-

The SaaS platform owns the merchant relationship and the data

By embedding payments, you are placing your platform between merchants and the financial system. A position like this gives you access to information, like transaction data, that is usually invisible to processors and banks. Such data can give you valuable insights into how you can expand or improve your services, as well as help you understand your customers better.

-

Enhanced compliance and risk management

Compliance is non-negotiable if you want to ensure a secure payment experience for your merchants and shoppers. Working with an infrastructure partner eliminates the need for you to set up a compliance posture for your payment system, which entails quite a series of steps from verifying merchant identities to managing disputes.

This is also where the distinction between embedded payments and the wider embedded finance umbrella becomes practical. Payments are one of the cornerstones of businesses. It’s not just about cash flow, but also about fostering the right business practices and building partnerships. If you can get this operational layer right, strategic moves will feel more natural than overwhelming. We explore that progression in Beyond Embedded Payments: How Vertical SaaS Platforms Expand Their Fintech Stack.

Is your software platform ready for embedded payments?

Readiness is less about company size or stage and more about workflow fit. The global embedded finance market reached $145 billion in 2025 and is projected to grow at a 33% CAGR through 2034, so for most vertical SaaS platforms, the question is no longer whether to embed payments, but when.

A great way to know if your platform should start embedding payments is by looking at your merchants. How are they handling transactions? How do they resolve payment-related issues? Are they reaching out to you or seeking new features like invoicing or customer portals? These are just some of the things you can look into if you want to check if your platform is ready for embedded payments.

Getting started with embedded payments

Embedded payments cover transactions within a business through the following products:

- Pay In – movement of money into a business

- Pay Out – movement of money towards vendors, suppliers, etc.

- Pay Ops – operational tooling that deals with pricing, reporting, dispute management, and underwriting controls

Accepting payments is usually the starting point for most vertical SaaS platforms aiming to embed payments. Once these transactions become routine and start bringing in volume, the other products can be easily stacked on top of them.

But it’s worth noting that setting up two or three of these products at once can lead to challenges that may impact your operations. The best approach is simply to launch one product and start earning from it before adding another:

| Stage | Products to turn on | Why this stage |

| 1 | Payment acceptance (Pay In) | Generates the transaction data and merchant relationships that every later product depends on. Highest immediate revenue with the lowest implementation risk. |

| 2 | Accounts payable (Pay Out) | Highest-margin extension once virtual cards and rebate programs are added. Requires acceptance to be live first. |

| 3 | Operational tooling (Pay Ops) | Compounds margin on Pay In and Pay Out through pricing controls, billing, reporting, dispute management, and underwriting. |

| 4 | Adjacent financial products | Working capital, card issuing, business accounts, and embedded lending: the broader embedded finance layer. The right move once the platform has enough transaction history to underwrite responsibly. |

Enhancing embedded payments with Payabli

Embedded payments serve as the foundation on which embedded finance is built. With a smart approach and the right infrastructure partner, embedding payments and ensuring the efficiency of transactions will feel less challenging.

With Payabli’s embedded payments, your organization can focus on helping your platform own its payment system by prioritizing matters most for your merchants and consumers instead of rolling everything out simultaneously. Pay In, Pay Out, and the Pay Ops tooling underneath them all sit on a single API, one merchant record, and one revenue share, giving you the ownership, economics, and data we’ve talked about throughout this guide.

Best of all, that foundation is built to grow with you. The split you commit to on day one still holds as your volume scales, with no re-platforming down the road. Payabli runs on a transparent revenue share. We negotiate wholesale rates with backend processors and sponsor banks, you set the pricing for your merchants, and we share the spread. And when you’re ready to extend further up the embedded finance stack, your payments layer is already in place to support the journey.

Book a demo now and discover how you can change the payment experience for your customers.