Key Takeaways:

- Embedded B2B payments enables vertical SaaS platforms to bring the entire payment experience natively inside their product, capturing economics on both sides of money movement without full PayFac registration.

- The embedded B2B payments market is projected to grow nearly fourfold by 2030, shaped by demand for integrated workflows and the decline of paper-based payments.

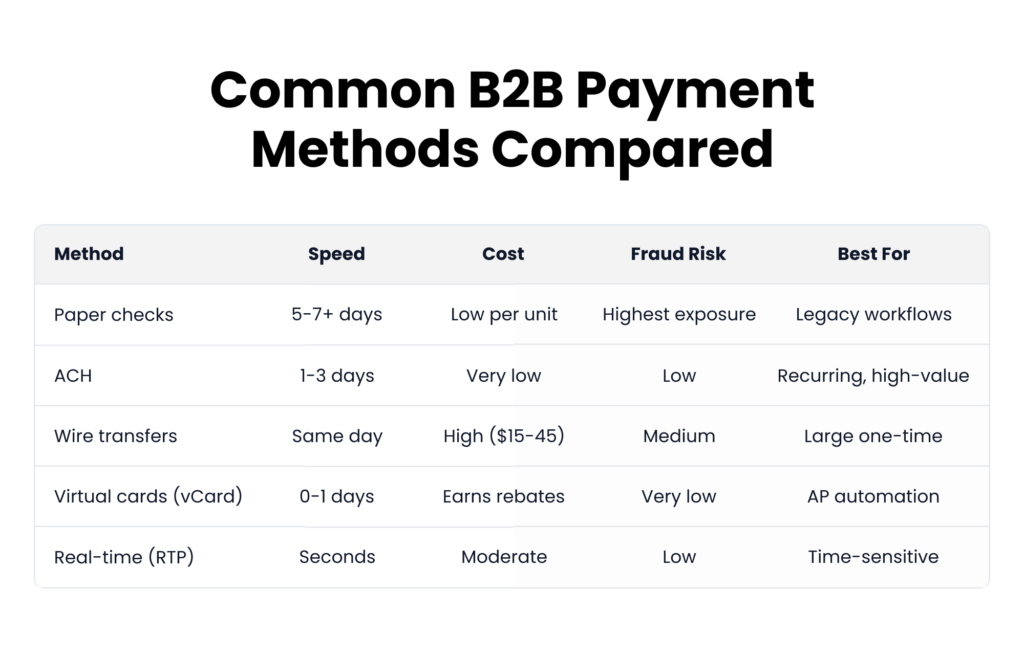

- The fastest-growing B2B payment method is virtual cards, with transaction volume projected to grow from $3 trillion in 2024 to $11 trillion by 2028, yet they represent only 2% of accounts payable transactions today.

- Embedding Pay In and Pay Out under a single unified API enables vertical SaaS platforms to capture both sides of money movement while building deeper customer stickiness.

B2B transactions still rely on manual invoicing, paper checks, and disconnected systems. More than half of all B2B invoices are currently overdue, and the downstream effects (reconciliation failures, delayed cash flow, and strained supplier relationships) are symptoms of the same root problem: payments that operate outside the software where business actually happens.

Vertical SaaS platforms that embed payment acceptance (Pay In) and accounts payable (Pay Out) directly into their product don’t just add a feature. They remove the friction that’s costing their customers real money and unlock a revenue stream that scales with every transaction.

Embedded B2B payments address this by integrating payment capabilities directly into the software platforms businesses already rely on. Instead of toggling between third-party payment tools, portals, and accounting systems, payments happen inside the workflow. This blog covers what embedded B2B payments are, why the market is accelerating, and what to evaluate in an infrastructure partner.

What Are Embedded B2B Payments?

Embedded B2B payments refers to bringing the entire payment experience natively inside the software platforms businesses already use. Through a PayFac-as-a-Service model, your platform captures the economics and controls the experience end to end, with no full PayFac registration required. Rather than context-switching to separate tools, all money movement happens inside the workflow, under your brand, on your terms.

For vertical SaaS platforms, embedded payments are often the foundation of a broader financial services strategy that can expand to include lending, insurance, or banking services over time.

When a property management company logs into its platform to collect HOA dues and then opens a separate banking portal to pay a vendor, those are disconnected B2B payments. With embedded B2B payments, both transactions happen inside the same platform, with the invoice, reconciliation, and payment all connected.

When working with the right payment infrastructure provider, embedded B2B payments can cover both sides of money movement for your platform. On the acceptance side (Pay In), merchants collect via cards, ACH, checks, and digital wallets. On the disbursements side (Pay Out), they pay vendors through ACH, wire transfers, virtual cards, and real-time payments (RTP), generating interchange revenue on every vendor payment. Pay Ops, the operational layer connecting both, handles underwriting, risk management, reconciliation, reporting, and compliance across the full payment lifecycle.

The key distinction in B2B payment workflows is that transactions involve invoices with multi-party approvals, large dollar amounts, payment terms, and compliance obligations that require purpose-built infrastructure to manage.

To explore how vertical SaaS platforms are layering additional financial products on top of payments, see Beyond Embedded Payments.

Why embedded B2B payments are one of the highest-value opportunities for vertical software platforms

Embedding payments isn’t just a feature add. It’s a revenue stream that grows with every transaction processed on your platform. Larger transactions, longer customer relationships, and deeper workflows makes embedded B2B payments one of the most significant monetization opportunities in vertical software platforms today.

- New revenue streams on both sides of the money movement. Embedded B2B payments unlock transaction-based revenue across Pay In and Pay Out, two channels most platforms leave on the table. On the Pay In side, every card payment, ACH transfer, or digitized check collected through your platform generates transaction revenue. On the Pay Out side, virtual cards are among the highest-margin disbursement methods available, generating interchange revenue on every vendor payment, often exceeding 100 basis points. Virtual cards represent just 2% of accounts payable transactions today, while 80% of buyers prefer them (Tearsheet). That gap is the opportunity.

- Larger transactions mean more revenue per payment. B2B transactions routinely run into thousands or tens of thousands of dollars. A platform processing a $50,000 vendor payment captures significantly more per transaction than one handling a lower-value payment. The underwriting and risk models that support those larger amounts also deepens the value your platform delivers, giving businesses meaningful financial controls built directly into their workflow.

- Better data makes your platform stickier. B2B payments generate rich transaction data: remittance details, invoice matches, ledger entries, and purchase order records. Surface that through reconciliation feeds and Level II/III transaction support, and your platform becomes the financial system of record your customers won’t switch away from.

- Faster onboarding and simplified compliance. The right embedded payment infrastructure provider handles KYB verification, underwriting, and risk monitoring natively, so your team can focus on the product and your customers can start transacting quickly, without the friction of managing it separately.

- More control over the customer experience. When payments live inside your platform, you control the full experience. Branded payment flows, configurable payment terms, automated reminders, and real-time reporting all happen inside your product, not in a third-party portal your customers have to navigate.

The Market Opportunity: Why Now?

The market is massive, underpenetrated, and moving fast. Embedded B2B payments are growing at a 25% CAGR, projected to reach $15.6 trillion by 2030 (Edgar, Dunn & Company). According to PYMNTS Intelligence, 62% of businesses now expect ERP integration for their accounts payable solutions, and 36% of executives identify adopting in-platform payment capabilities as a top priority for staying competitive. For vertical software platforms, that pressure is an opening: businesses are actively consolidating financial operations inside the tools they already use.

The shift away from legacy payment methods is accelerating. In September 2025, the U.S. Treasury moved away from paper checks for most disbursements, and similar digital-first mandates are emerging globally. Virtual cards and real-time payments are replacing manual AP workflows, and AP automation adoption is driving disbursement volume onto higher-margin rails.

A longer-term force is also taking shape: agentic fintech. As AI agents execute financial workflows autonomously, the platforms that have already embedded payments will be positioned to absorb that automation layer naturally. Payments won’t just be a feature your customers use. They’ll be a function AI operates on their behalf, inside your platform.

Vertical SaaS platforms that move now, embedding Pay In, Pay Out, and Pay Ops under a single unified API, are building payment businesses, not just adding features.

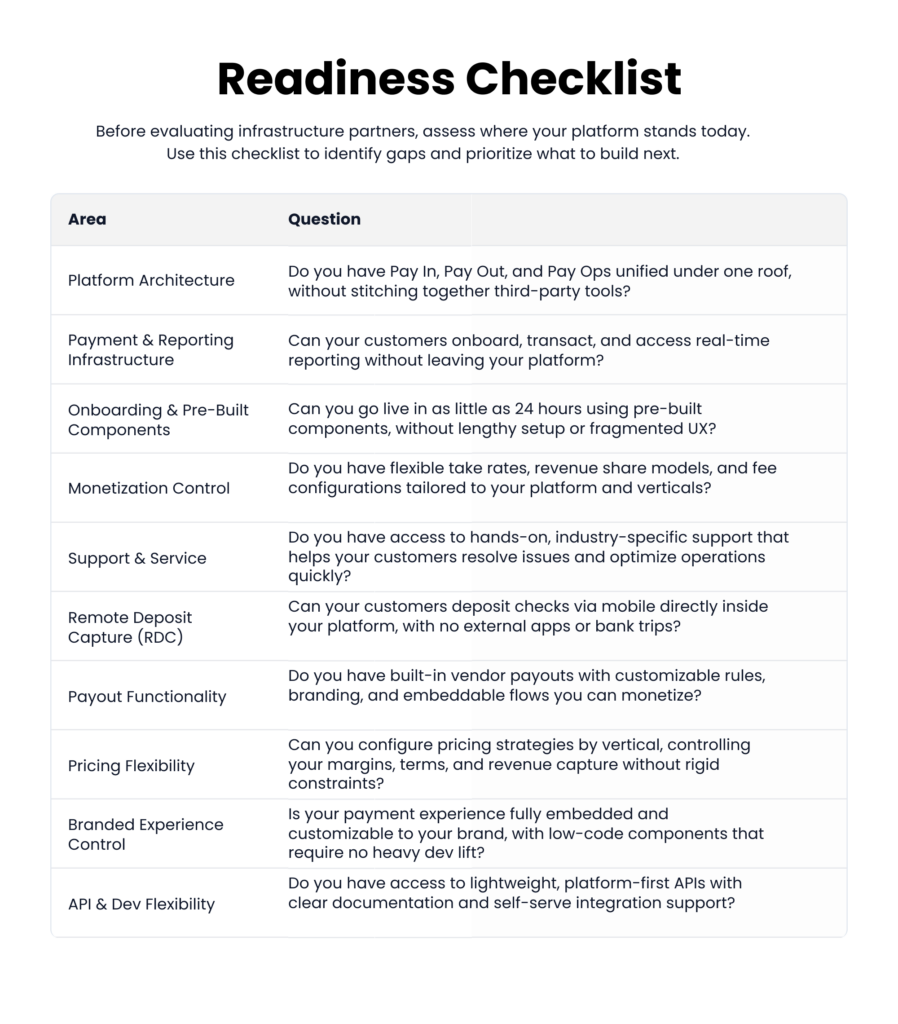

What to evaluate in a B2B Payments infrastructure partner

B2B embedded payments require capabilities that go well beyond standard payment processing. The right partner should be purpose-built for these workflows.

Vertical-specific payments expertise

Payment workflows aren’t generic, and neither is the infrastructure that should support them. A construction platform managing progress billing and subcontractor disbursements has fundamentally different requirements than a property management platform collecting rent and HOA dues, or a healthcare platform navigating patient billing and insurance reconciliation.Your infrastructure partner should be purpose-built for vertical software, not a horizontal processor retrofitting generic tools to your use case.

Integration that meets your engineering team where they are

Embedding payments should accelerate your product roadmap, not slow it down, and the right partner gives you optionality based on where you are in your payments journey. The right partner supports a crawl, walk, run approach: launch with pre-built tools, embed with configurable components, then build a fully custom experience when you’re ready. And if you’re starting with Pay In but want to layer in Pay Out down the road, that expansion should be straightforward, not a separate conversation.

Compliance built for B2B payment workflows, not bolted on after

B2B payments carry requirements that go well beyond standard PCI DSS and NACHA obligations. KYB verification for onboarding multi-entity merchants, positive pay for check fraud prevention, and Level II/III data submission for interchange optimization are baseline B2B expectations, not edge cases. Look for a partner that handles these natively and engages directly on underwriting, not one that hands you a questionnaire and walks away. That distinction keeps your engineering team focused on your product roadmap and your compliance posture intact.

Dedicated support and implementation partnership.

The implementation phase is where most embedded payments programs succeed or stall. The right partner assigns a dedicated team, not a ticketing queue, from onboarding through launch and beyond. The right partner understands your platform before integration begins, not just after something breaks. Proactive monitoring, clear escalation paths, and a partner invested in your long-term success, not just your go-live date, are the markers of a provider worth trusting.

Merchant adoption, conversion, and monetization strategies.

Embedding payment capabilities is only the beginning. Revenue is directly tied to how many customers activate and how deeply they engage. Look for a partner with proven merchant adoption playbooks and launch checklists, friction-reducing onboarding flows, and in-platform prompts that drive activation at the right moment. The right partner works alongside you to increase payment volume and deepen engagement across your customer base, so your payments program compounds as your platform grows.

From Payment Features to a B2B Payments Business

Platforms that embed B2B payments capture margin on both sides of every transaction, build a revenue stream that scales with their software, and deepen the merchant relationships that drive long-term retention. The opportunity ahead is significantly larger than what has already been captured.

Payabli works with vertical SaaS platforms across property management, HOA, field services, construction, education, healthcare, legal, and government to design and launch B2B payment strategies specific to their vertical. If you’re exploring how to embed and monetize B2B payments into your platform, Book a demo today.