Key takeaways:

- Embedded payments give vertical SaaS platforms full control over merchant onboarding, pricing, branding, and data, whereas integrated payments hand those functions to third parties.

- Under an integrated model, a platform processing $50 million in annual volume may earn only 5 to 15 basis points in referral fees. In contrast, under embedded payments, the same volume can generate 5 to 10 times more revenue.

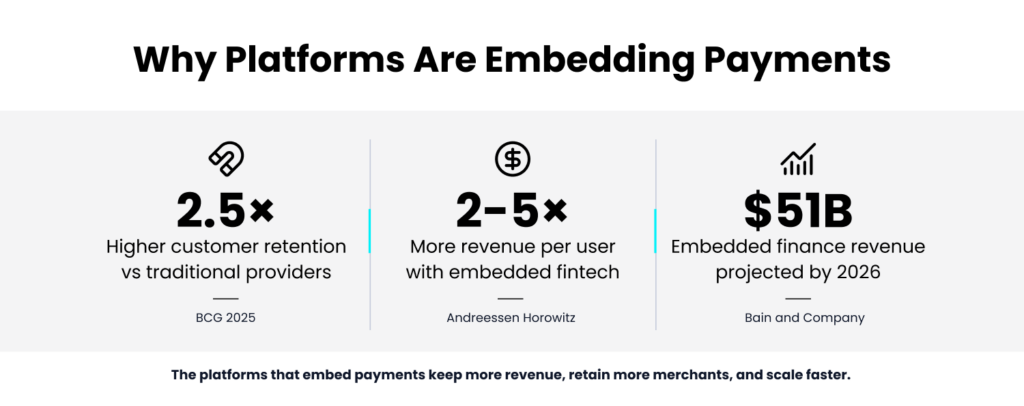

- By using embedded payment strategies, SaaS platforms can retain customers at 2.5 times the rate of traditional payment providers, and their merchants embrace 18% more value-added services (BCG 2025).

- Vertical SaaS platforms can achieve PayFac-Level economics without full PayFac registration. PayFac-as-a-service provides the same margin control and merchant ownership while eliminating the compliance burden.

In the ever-evolving world of vertical SaaS platforms, choosing the right payment strategy can be a make-or-break decision, not just for platform growth but also for customer experience and monetization. Two terms often used in this conversation are integrated payments and embedded payments. While they may sound similar, the difference is profound, and so are the benefits of getting it right.

In this blog, we’ll break down the distinction between integrated and embedded payments, examine the market data behind each approach, and explain why embedded payments are the gold standard for vertical SaaS platforms looking to scale efficiently and profitably.

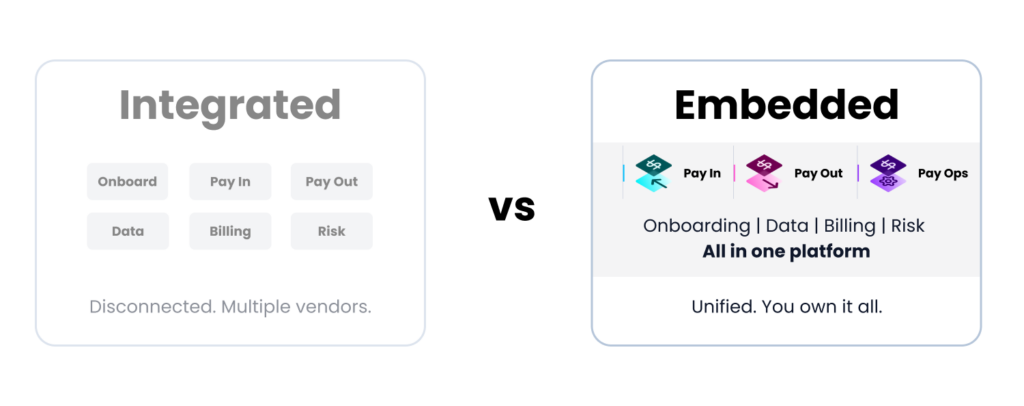

What are integrated payments?

Integrated payments refer to the approach where a SaaS platform connects to a third-party payment provider (such as Stripe, PayPal, or Authorize.Net) using APIs or plug-ins. While the integration enables payment functionality, the actual experience, like merchant onboarding, transaction monitoring, or settlement, is still handled largely outside of your platform.

SaaS company’s control over the pricing, user experience, and monetization is limited by this model. Software platforms now manage 60-70% of their clients’ payment processing contracts according to a 2025 BCG report on merchant services. Platforms using integrated payment models often give up this control to the third-party providers, along with the linked revenue.

What are embedded payments?

Embedded payments go a step further by deeply integrating the entire payment experience within the SaaS platform. From merchant onboarding and KYC, to accepting payments, managing payouts, and delivering insights, everything happens natively in the software interface.

Fully embedded payments within your platform mean that merchants onboard, transact, and access real-time reporting without ever leaving your software. This ensures a seamless, consistent experience that feels like a natural part of your product, not an external add-on.

This model is often powered by becoming a Payment Facilitator (PayFac) or by partnering with a PayFac-as-a-Service provider.

The financials for embedding payments are well documented. According to Bain & Company, the embedded finance revenue is projected to increase from $21 billion in 2021 to around $51 billion by 2026. The embedded payment market alone reached $24.7 billion in 2024 and is growing at a 30.3% CAGR through 2034.

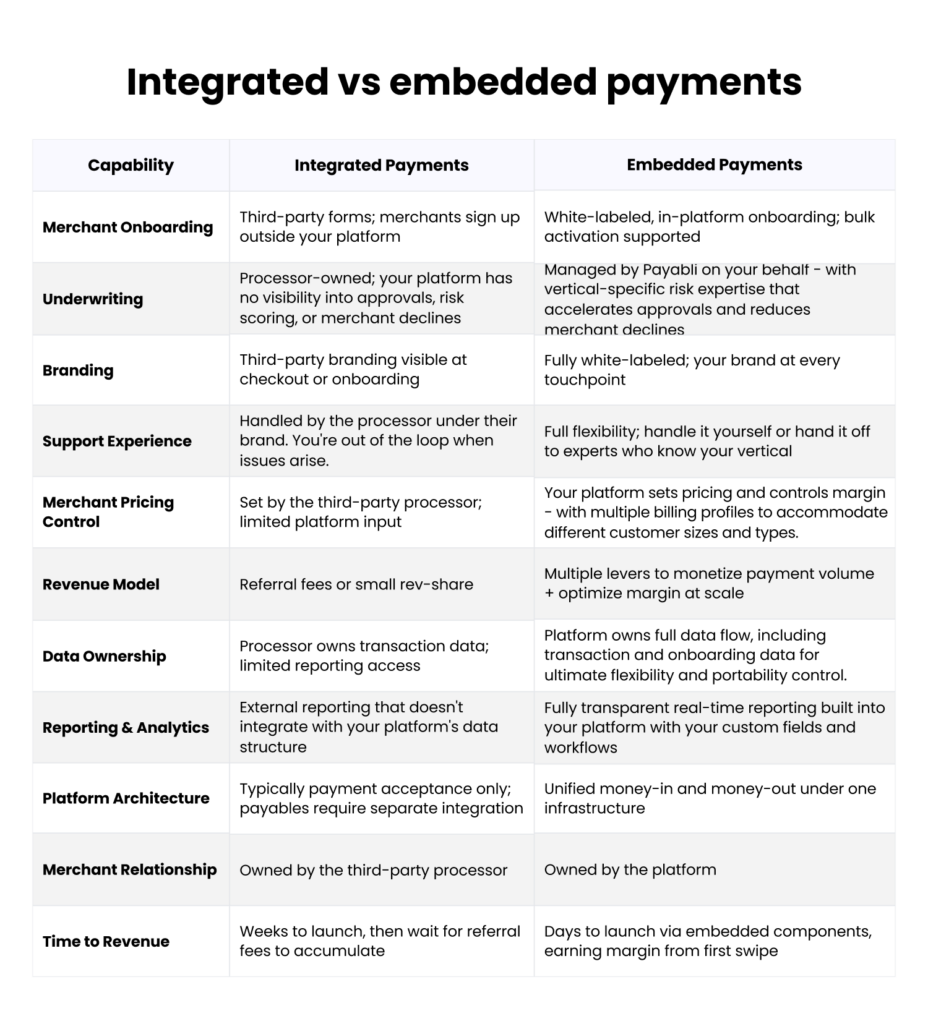

Integrated vs. embedded payments: A side-by-side comparison

The significant difference between the two models extends across onboarding, revenue, data ownership, branding, and compliance. The table below summarizes how each approach performs on capabilities that matter most to platform administrators.

For a practical walkthrough of what it takes to go live with embedded payments, see Payabli’s Embedded Payments Launch Checklist.

Why do embedded payments win on user experience?

For vertical SaaS platforms, user experience is everything. Embedded payments dramatically enhance the merchant journey and unlock new business value in ways integrated payments simply can’t.

1. Frictionless onboarding

Say goodbye to third-party forms and redirection. Merchants can sign up and start accepting payments right inside your platform, often within minutes. Payabli’s Creator tool enables platforms to apply branded onboarding without any coding, further reducing time to first transaction.

2. Unified UI and experience

The payment flow stays consistent with your platform’s design. This creates a branded, trustworthy experience for your users.

3. Faster time-to-revenue

While integrated options may involve multi-day approval processes, embedded payments often enable instant and/or bulk onboarding and activation, meaning your users start transacting sooner. This speed directly translates to faster payment volume growth for platforms serving high-volume verticals.

4. Deeper data visibility

With embedded payments, your platform owns the entire data flow, transaction history, user behavior, and payout activity, which means better analytics and smarter customer engagement.

5. New revenue streams

Rather than handing over valuable payment margins to third parties, you capture a share of the transaction revenue. This high-margin income can transform your SaaS business model. According to Andreessen Horowitz, revenue per user can be increased 2 to 5 times by adding embedded payments.

6. Streamlined compliance (with the right partner)

PayFac-as-a-Service solutions help you deliver a native experience without taking on the full regulatory or administrative burden of being a registered PayFac yourself.

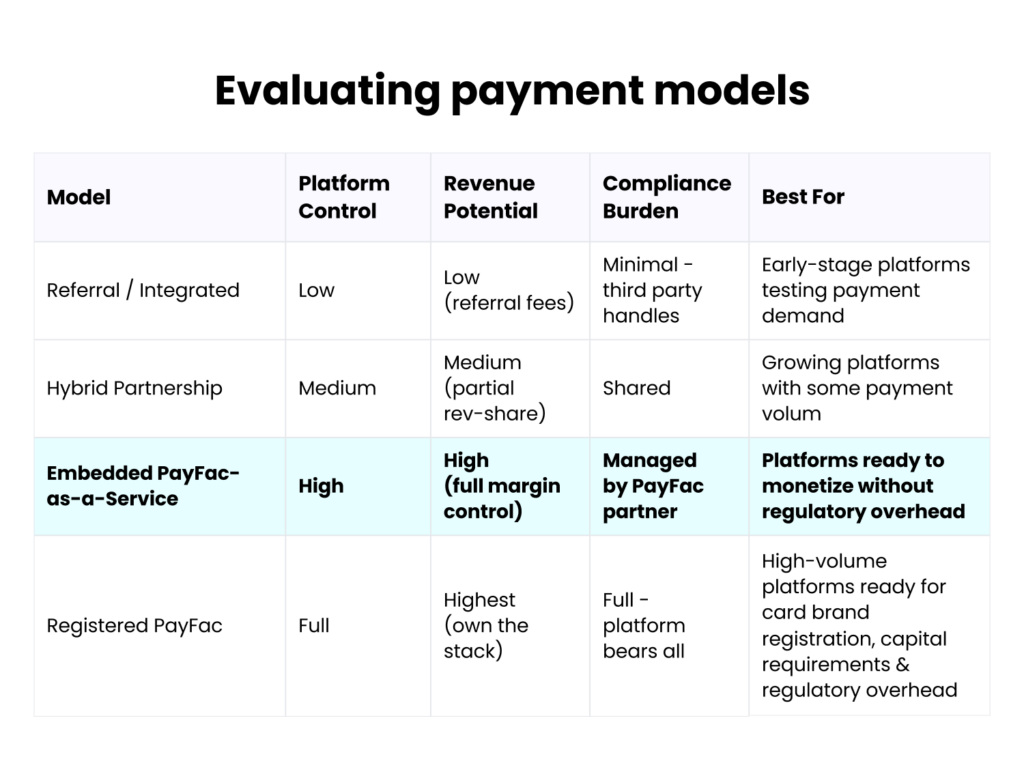

How to evaluate your payment model

The perfect payment model depends on your platform’s technical resources, stage, and growth goals. Not every platform is prepared for full PayFac registration, but most can benefit from PayFac-as-a-Service immediately. The table below outlines the four primary models and what each requires.

What to look for in an embedded payments provider

If you’re ready to embed payments into your SaaS platform, the provider you choose will have a massive impact on both your product experience and your bottom line. Here are four key things to look for:

1. Unified Pay In and Pay Out capabilities

A common limitation among many embedded payment providers is the inability to support both payments and disbursements under one roof. This can create friction when trying to manage sub-merchants, service providers, or vendor payouts. Choose a provider that bridges both sides of the money movement, ensuring faster settlement, seamless fund distribution, and better cash flow control. The ability to earn revenue on both inbound and outbound payment flows, including virtual card rebates on vendor payouts, is what distinguishes a payments feature from a payments business.

2. Flexible integration options

Your development team shouldn’t have to force-fit your platform into rigid SDKs or templated flows. Look for providers that offer modern, modular APIs, webhooks, and event-driven architecture, and clear documentation and sandbox environments. This allows you to tailor the payment experience to your platform’s design and business logic.

3. Hands-on, expert support

Payments can be complex, but your journey shouldn’t be. The right provider offers proactive, strategic guidance from discovery to go-live, and everything in between. That includes technical integration support, merchant onboarding optimization, compliance and risk workflows, and ongoing product and go-to-market strategy. Unlike most providers, the right partner will also offer merchant-level support.

Beyond launch, you should expect responsive, hands-on support from experts who understand your industry. The right partner will help you and your customers resolve issues quickly, optimize operations, and provide guidance tailored to your vertical, whether you’re serving contractors, gyms, law firms, or property managers.

4. Cost and pricing transparency

A strong payment partner doesn’t just present pricing, they help you understand it and turn it into a strategic revenue stream. Look for transparent rates and no hidden fees, flexible monetization options, simple easy-to-read billing, tailored pricing strategies by vertical, flexible pricing structures, and granular monthly statements to optimize margin at scale.

For vertical SaaS platforms, payments are more than a back-end utility, they’re a strategic lever for growth, retention, and monetization. While integrated payments may offer a quick start, embedded payments create long-term value through a smoother user experience, stronger brand ownership, and deeper monetization opportunities.

Choosing the right partner is just as important as choosing the right model. With the right embedded payments provider, your SaaS platform won’t just process payments, it will own them.

From integrated payments to a payments business

Most vertical SaaS platforms started with an integrated payment model because it was the fastest path to offering payments. But as your merchant base grows, the gap between what integrated payments deliver and what embedded payments unlock becomes harder to ignore: more revenue per transaction, full brand ownership, and a merchant relationship you control. See how the two models stack up in our full comparison table above.

Payabli helps platforms make that transition. Whether you are moving off a referral model, replacing a fragmented multi-vendor setup, or embedding payments for the first time, Payabli’s unified Pay In, Pay Out, and Pay Ops infrastructure gets you live in weeks with PayFac-Level economics.

Book a demo to see how platforms like Sunbound made the switch.